In my more than 30 years of professional experience in the financial industry, I have witnessed crises of various origins and natures. However, I must admit that I have rarely faced a situation as uncertain and difficult to interpret as the one our country has been experiencing since late 2019. As a result of the events that occurred in October of that year and the subsequent health and economic crisis caused by COVID-19, the Central Bank developed a daily economic uncertainty measure called the “Twitter-Based Economic Policy Uncertainty Index for Chile.” Based on information published on 15 official Twitter accounts belonging to the country’s leading television, print, and radio news outlets—with a potential reach of 25.7 million users—its purpose is to provide decision-makers with an additional indicator to complement their usual monitoring tools. This is undoubtedly a necessary tool, given the uncertainty associated with the pandemic and the process of institutional changes the country has initiated.

In an effort to better understand this situation and the policy measures being proposed to address it, I have carefully read the campaign platforms of the candidates from the two political blocs who will be competing in the primary elections in the coming days. At times, it is difficult to understand how, when faced with the same problem, it is possible to find radically different solutions depending on the ideological stance of the party or movement supporting a given candidate. However, the tax proposals contained in some of these platforms have particularly caught my attention.

With what appears to be a lack of understanding of our tax system, there is talk of comparatively low and insufficient tax revenue, an unfairly distributed tax burden, and other concepts that reflect an ideological bias in the analysis and proposals.

Any proposal to amend the current tax system must take into account certain essential principles, such as the legality of taxation, tax equality or equity, the non-confiscatory nature of taxes, simplicity that facilitates tax collection, and sufficiency that ensures the necessary resources to finance public spending.

The candidates have expressed their intention to increase tax revenue by 5% to 10% of GDP—or rather, by an additional 25% to 50% of what we currently collect. This inevitably raises the question: Which taxes do they plan to increase? By how much? Or which new economic activities do they intend to tax?

The cold, hard numbers show that our country’s tax revenue amounts to 20.7% of GDP, while the average for OECD countries is 33.8% (of GDP), with this percentage including revenue from VAT, personal income taxes, and social security contributions, and social security contributions. Seen this way, it may seem to any impartial reader that there is still room to narrow the tax gap that apparently exists with the countries we compare ourselves to.

However, this assessment is not entirely accurate, for reasons including the fact that in OECD countries, social security is a pay-as-you-go system (9.2% of GDP), and individuals’ contributions to the system are higher than those in our individually funded model (1.5% of Chile’s GDP).

For this reason, and before making these kinds of comparisons, I believe it is necessary to clarify some points regarding the information used for these calculations. For example, if we were to exclude—in the case of Chile—the defined-contribution system and, in the case of the OECD, the pay-as-you-go systems, since these cannot be compared, the figures show that our country’s revenue would be 19.6% (GNP), and the OECD an average of 25.1% (GNP)—figures that are, incidentally, very different from the percentages and numbers presented in these programs.

It is therefore interesting to take a closer look at the taxes we pay in Chile and see if there is indeed room to improve tax collection.

A simple review of the official data leads us to conclude that, with regard to VAT Chile is about average; however, it is well above average when it comes to corporate taxes.

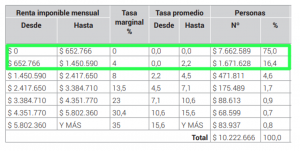

One area where there is a significant gap in tax revenue is personal income tax. Chile collects the equivalent of 1.4% of GDP from this source, while the average for OECD countries is 8.3% of GDP. How can this gap be explained?

There are two notable facts that help explain the low revenue from this tax: one is the size of the tax-exempt bracket, which covers 75% of potential taxpayers; the other is the source of the revenue, 60% of which comes from individuals in the highest tax brackets.

Given the current political landscape and social climate, it seems unrealistic to consider reducing the tax-exempt threshold and imposing taxes on lower-income individuals who are dissatisfied with the services provided by the government in areas such as housing, health care, and education, among others.

In an election year, it’s no surprise that the issue of our tax system is once again taking center stage. Given the proposals on this matter and a long list of “social rights” that there is a consensus on guaranteeing, it seems clear that the country will face greater budgetary pressures as a result of the need to finance these demands. The candidates’ platforms draw on a series of proposals that are hardly novel and whose implementation may have unforeseen consequences. Along these lines, there is talk of increasing mining royalties, imposing a capital gains tax, taxing foods that are harmful to health, eliminating tax exemptions, and other measures, the equity, efficiency, simplicity, and adequacy of which will need to be evaluated.

However, in this discussion, it seems prudent not to forget that we are part of a global, competitive world, where countries compete to attract new capital and investors are free to make the decisions they deem most appropriate. In the tense atmosphere the country is currently experiencing—one dominated at times by slogans and catchphrases—it seems prudent to reflect calmly on this and other issues of particular importance to the country we want to build.

Francisco Muñoz

Partner – Sales Director, FYNSA