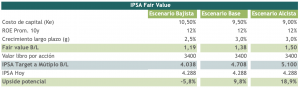

Our scenario assumes an IPSA target of 4,700 points. We base our projections on a relatively conservative scenario in terms of valuations, recognizing that the domestic outlook will remain challenging given the ongoing constitutional process and the presidential election this coming November, but that, given the magnitude and timing of monetary and fiscal stimulus measures, valuations that are already fairly discounted, and a favorable international environment (including the recovery in key commodity prices), these factors would offset some of the domestic political and electoral risks.

Looking ahead to the rest of 2021 and taking into account the new information available, there are reasons to be a little more optimistic (or, if you prefer, “less pessimistic”).

- While we recognize that some sources of uncertainty will remain, following the results of last weekend’s presidential primaries—in which the most extreme rhetoric was defeated and the idea of defending institutions is gaining ground— we believe this opens up some room to focus more on economic recovery, the reopening of businesses, and improvements in corporate earnings. Thus, we could see a couple of slightly calmer months (leading up to the presidential election) that would allow the IPSA to reverse some of the sharp decline already priced into valuations, as political headwinds will ease somewhat and the market will be able to move more in line with fundamentals.

- The external environment will remain favorable, with copper prices expected to continue rising, increased global liquidity, and a highly expansionary fiscal policy that is heavy on raw materials—all of which are key indicators that could lead to higher capital gains on the local stock market.

- In terms of public health, with more than two-thirds of the population fully vaccinated and the progress of the “Step-by-Step” plan, the economic reopening has been gaining momentum. So far, the country is in a privileged position due to the availability of vaccines, thanks to the government’s efforts, which have served as an example for other countries in the region and even for several developed nations. This will naturally help accelerate the recovery of our economy.

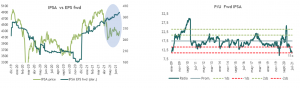

- All of this leads us to believe that, on the one hand, we could see a better-than-expected recovery in corporate earnings and, on the other hand, there could be room for some expansion in P/E ratios.

In terms of strategy, we favor stocks that we believe are undervalued (value), of high quality (solid financial position), and have growth potential. By sector, we are focusing on commodities, banking, retail, and real estate.

- We expect the favorable trends in the commodities sector to continue going forward, as the combined fiscal and monetary stimulus—which far exceeds the measures taken during the financial crisis—coupled with greater stability in the Chinese economy, are tailwinds for demand in the sector. This, combined with the expected weakness of the dollar and certain supply shocks related to COVID-19, should support further price recoveries.

- We believe that sectors such as retail, shopping, and banking would benefit the most from fiscal stimulus through government bonds and ample consumer liquidity, coupled with the economic reopening driven by progress in the vaccination process.

If you'd like to see more details about this article, click here: Domestic Equities