Without a doubt, 2021 has been a good year for risky assets, but it has also been a very uneven year in terms of regional performance. While U.S. stocks have returned 25%, markets such as Europe and Japan—within the developed markets—have underperformed, posting returns of +10% and +1.49%, respectively. Not to mention the poor performance of emerging markets (-4.35%), which were affected by financial and regulatory crackdowns in China and a slowing economy.

What stands out about this trend is that while earnings growth for U.S. companies is on track for a solid +45% in 2021, markets such as Europe and Japan are outpacing that at +65% and 48%, respectively. Even emerging markets are projected to show earnings growth of close to 60% in 2021. In other words, non-U.S. markets have been affected by a “multiple compression” rather than by disappointing corporate performance.

The fact that the S&P 500 is leading stock market returns can be explained primarily by the U.S. economy, which has proven to be a reliable source of growth. It has emerged from the pandemic stronger than anywhere else, thanks to highly expansionary monetary and, above all, fiscal policies, while elsewhere, progress has been slower. China’s GDP growth has slowed, and in Europe, a surge in COVID-19 infections has led to some restrictions on business activities.

The question that follows, then, is: Will this trend continue in 2022?

A significant part of the answer has to do with the course of the pandemic. Last week, we argued—in light of the emergence of the Omicron variant—that its potential effects were likely being exaggerated; while Omicron is probably more transmissible, early reports suggest it may also be less deadly, which would fit the pattern of the virus’s evolution observed historically. If these trends are confirmed, could the Omicron variant ultimately prove beneficial for risk markets, in the sense that it might hasten the end of the pandemic? If a less severe and more transmissible virus rapidly displaces the more severe variants, could the Omicron variant serve as a catalyst to transform a deadly pandemic into something more akin to seasonal flu? Such a development would be consistent with historical patterns (duration and number of waves) of previous respiratory virus pandemics, especially given the widespread availability of vaccines and new therapies that are expected to be effective against all known variants (Pfizer, Merck).

We believe that by 2022, the pandemic will be largely subsiding, supported in part by high vaccination rates that should become more widespread and regionally distributed, which should allow the global growth gap to narrow. As we noted, the U.S. economy has more than recovered, but other countries still have ground to make up—and eventually will. Much of Asia’s sluggishness is attributed to China’s slowdown and not sufficiently to the lingering effects of the pandemic in the region. In this regard, the fact that China adopted language supporting the economy and the real estate sector at the recent Politburo meeting strikes us as the first step toward reversing this trend in 2022. Meanwhile, Europe has never fully reopened, and fiscal stimulus from the European Union’s Recovery Fund is in the works. The United States could still lead, but the race will be closer.

From a tactical perspective, we are optimistic about stocks, given strong economic growth, solid earnings, and low bond yields.

Global economic growth is likely to remain above trend in 2022, andwe believe that equities in the eurozone and Japan, U.S. mid-cap stocks, the global financial sector, commodities, and energy stocks will benefit from this.

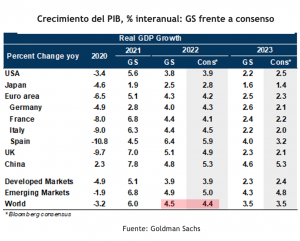

Global corporate earnings are projected to grow by 10% in 2022. Within this forecast, we believe cyclical stocks will post the highest rates of earnings growth, given their greater sensitivity to economic growth. In particular, we favor the eurozone and Japanese equity markets, the global financial sector, and U.S. mid-cap companies. We also favor commodities and energy stocks, which will also benefit if inflation proves more persistent than in our base-case scenario.

For Japanese equities, we expect further easing of COVID-19 restrictions to boost both economic growth and investor confidence in Japan. The government of the new prime minister, Fumio Kishida, is expected to push through a fiscal spending package amounting to approximately 4% to 5% of GDP. Monetary policy is also likely to remain relatively expansionary and contribute to further yen weakness. The TOPIX index is trading at 14 times 12-month forward earnings, making it cheap relative to the multiples of 18.6 times and 21.1 times for the MSCI All Country World Index (ACWI) and the S&P 500, respectively.

After underperforming U.S. stocks every year for the past decade, eurozone equities are one of our top picks for 2022. The eurozone market is cyclical, so it is well-positioned to benefit from the resolution of supply chain issues and inventory restocking. Investors’ current exposure to the region is light (only 3% of equity positions are in MSCI EMU stocks, compared with the eurozone’s 9% weighting in the MSCI ACWI Index). In the coming months, eurozone equities should be supported by expansionary monetary and fiscal policy, as well as strong GDP growth and corporate earnings.

The global financial sector has historically performed well when yields have risen slightly. We expect yields on 10-year U.S. Treasury securities to reach levels closer to 2% in 2022. Fundamentally, we believe that the financial sector’s earnings should benefit from stronger loan growth and improved credit quality, as well as the release of loan loss provisions.

We expect commodity prices to stabilize in 2022. However , many commodity-related stocks have not yet priced in a prolonged period of high prices. For example, it is estimated that energy sector stocks are still only pricing in a long-term Brent crude oil price of 60 USD/barrel.

We also see value in industrial metals, particularly copper, which are expected to benefit from the transition to net-zero carbon emissions. This could lead to a more active approach to commodity allocation, which in turn would offer investors protection in the event that commodity supply issues lead to more persistent inflation.

Decline in investment

Humberto Mora

FYNSA Strategy and Investments