We reiterate our view that markets are likely to experience a continued and significant internal rotation toward the end of the year, driven by a rise in bond yields and the end of the yield curve flattening. Many are concerned about the sustainability of the rotation, as growth prospects are viewed as mixed at best, and the rotation is unlikely to persist if we experience an energy/inflation/Fed shock, which would ultimately depress growth and trigger a reversal in yields.

In our baseline scenario, we will continue to see higher inflation, but also stronger growth. We note that, while inflation surprises remain on the upside, economic surprises also appear to have bottomed out—a trend that is most evident in the U.S., but we expect the same for the Eurozone and China.

We believe that the headwinds to growth that have been present in recent months—the slowdown in China, the resurgence of COVID-19 cases linked to the Delta variant, a loss of consumer confidence, and the slowdown in job growth—are easing; therefore, given current CESI (economic surprises) levels, we are likely to see a rebound toward the end of the year.

We therefore believe that the driving force behind the rotation will be rising bond yields. U.S. bond yields have risen more than 40 basis points from their August low, and we believe there is further downside ahead, as we expect part of the gap between inflation breakeven rates and bond yields to begin to narrow.

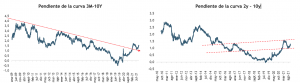

Not only are yields rising, but the slope of the yield curve has also steepened.

Which sectors are benefiting in this context? In general, the more “value”-oriented sectors that are used most directly as a hedge against inflation (the energy sector) and commodities in general, but also the financial sector, given the steeper yield curve. Furthermore, the financial sector is significantly outperforming earnings estimates in Q3 2021, with positive surprises of +2.8% in revenue and +21% in profits, and relative valuations compared to the broader market remain quite attractive.

Decline in investment

Humberto Mora

Strategy and Investments