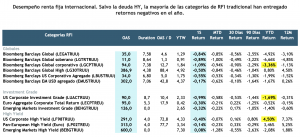

This year marks the first time in nearly a decade that bond investors have experienced significant negative returns.In part, the massive sell-off in bonds was the result of receding coronavirus risks and a strong economic recovery, and in part the consequence of high inflation risks and the potential unwinding of highly accommodative monetary policy. In principle, our forecasts for next year suggest that yields—particularly on longer-duration bonds—are likely to turn negative again.

With the pandemic largely behind us, interest rate markets next year will likely be driven by inflation data and how central banks choose to respond.These factors will need to be weighed alongside the tightening of labor market conditions, which, all else being equal, implies higher equilibrium yields.

While we do not expect the major developed-market central banks (particularly the Fed and the ECB) to raise rates very aggressively next year, high inflation and strong growth will likely lead markets to anticipate this tightening, and yields should rise. Therefore, yields are likely to remain a source of downward pressure on sovereign bond markets, as they were in the second half of this year.

With this as our backdrop, let's move on to the strategy

When structuring a fixed-income strategy, there are key variables to consider: credit risk and spread levels, the trajectory of interest rates, duration risk, and liquidity.

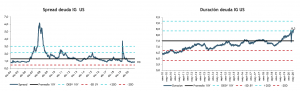

The current environment is particularly challenging for a fixed-income portfolio and more conservative risk profiles. Interest rates are at historic lows (therefore, rate risk is asymmetric), the duration of investment-grade (IG) fixed income is at record highs of over 8 years (therefore, duration risk is very high), and corporate spreads are at near-historic lows (offering little cushion against rate hikes).

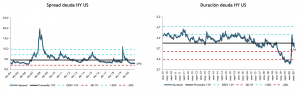

In particular, we do not see much risk of widening spreads given the positive macroeconomic environment, the favorable corporate outlook, and increased risk appetite; therefore, maintaining exposure to high-yield (HY) debt remains a good alternative, especially given its short duration. Emerging market (EM) debt may be an alternative, but it carries considerably higher risk, given the prospects of deteriorating macroeconomic and financial conditions in China and heightened inflation risks.

We also believe that the prospect of low yields will continue to fuel demand for illiquid segments, such as private debt markets, as well as for more complex instruments, such as structured products.

Decline in investment

But what should I do if I don't want to sacrifice liquidity and don't want to be exposed to the higher volatility of high-yield and emerging-market debt?

Fortunately, there are now active investment strategies on the market that are globally diversified, flexible in terms of duration, aim to generate the highest possible income with a limited level of risk, and seek to provide predictable dividend income.

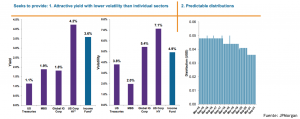

Simply put, they offer attractive returns with less volatility than individual sectors and predictable distributions.

These strategies essentially invest in all types of fixed-income securities. They include government bonds, corporate bonds (investment grade and high yield), emerging market debt (EMD), and securitized debt—all of which are liquid and very short-term, which is what allows for predictable coupon payments, in addition to being floating-rate debt.

Within this range of strategies, we highlight two funds:

PIMCO GIS Income Fund and JPM Income Fund

The first is a strategy that has met its objectives for more than a decade: that is, seeking value in the global fixed-income market while balancing returns with capital preservation goals.

The fund currently has a duration of 1.6 years and a YTM of 3.6%, and has posted a year-to-date return of 1.42% (as of the end of October), a 12-month return of 6%, and an annualized return of 5.3% over the past three years.

The second strategy employs an investment process driven by a globally integrated research process that focuses on analyzing fundamental, quantitative, and technical factors across all countries, sectors, and issuers.

The fund currently has a duration of 1.2 years and a YTM of 3.6%, and has posted a year-to-date return of 2.8% (as of the end of October), a 12-month return of 6%, and an annualized return of 5.5% over the past 3 years.

Humberto Mora

Strategy and Investments