There are two concepts that dominate the baseline scenarios for 2022. A return to "normality," assuming that the pandemic is behind us, and a "more volatile" year as a result of monetary policy normalization.

In our last newsletter of 2021, we commented that, in our opinion, 2022 will be the year of a full global recovery and the end of the global pandemic, thanks to the achievement of widespread immunity among the population and new therapies. We also noted that this would translate into a strong cyclical recovery, a return to global mobility, and a release of pent-up demand from consumers (e.g., travel, services) and corporations (inventory recovery, capital investment, and repurchasing), in a context where monetary policy will remain accommodative.

For this reason, we remain positive on equities, commodities, and emerging markets, and negative on bonds.

But some risks have emerged... The Fed is moving toward a "tougher" stance.

The December FOMC minutes portray "a Committee on track to remove monetary accommodation," which comes as no surprise to anyone. However, with regard to the expected path of policy rates, the minutes indicate that participants see rate increases "sooner or at a faster pace" than previously expected.

The minutes also indicated that participants continued to view mid-March as an appropriate end date for net asset purchases and therefore consistent with a first rate hike at the meeting that month.

However, what was new in the minutes, and also unexpectedly "hardline," were the clues given to the form of balance sheet normalization.While some lean toward the view that balance sheet assets will be depleted after the first rate hike, the general view was that asset sales would occur before takeoff in relation to the 2014-17 episode. In addition, it was generally considered that the pace of asset sales would be faster than in the last experience: as a reminder, last time two years passed between the first rate hike and the start of balance sheet contraction, so the Fed is now hinting that it could shorten this to less than nine months for balance sheet reduction to begin in 2022.

On the economic front, growth "remained strong, albeit with some nuances," reflecting increases in Covid cases and a "more gradual" resolution of supply chain disruptions."Many participants noted that new variants of the virus pose 'downside risks to economic activity and upside risks to inflation.'"

On the other hand, "most" participants considered that the economy could reach maximum employment "relatively soon if the recent pace of improvement in the labor market continued," and "several" participants noted that they "considered labor market conditions to be already largely consistent with maximum employment." "Some"participants noted that it might be appropriate to raise the federal funds rate "before maximum employment has been fully achieved," for example, "if inflationary pressures and inflation expectations were to rise materially and persistently." These comments again appear consistent with a rate hike in March.

In particular, we believe that the risks to growth are limited, but not so the risks to inflation, given that stress on supply chains remains at peak levels.

Against this backdrop, we believe that markets will be vulnerable to a faster rise in sovereign bond yields at the start of this year.

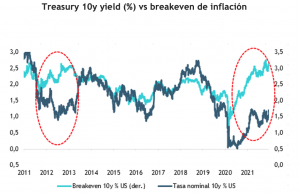

In fact, 10-year sovereign rates in the US are already trading at 1.75%, a key level as it was the pivot point throughout 2021.After that, rates have room to easily rise to 2.2%.

It is not that a rate at these levels is particularly problematic in terms of equity valuations, as our estimates for the S&P 500 this year at 5,000 points already factor in a 10-year Treasury yield closer to 2.0%, but we are concerned about the speed of this eventual movement. In other words, rather than the level of interest rates, the market is stressed by rapid movements over short periods of time, which may end up being the case, given the tougher tone set by the Fed, inflationary risks, and a tight labor market.

And what about the actual rates?

Something remarkable has happened at the start of this year: while real Treasury rates had been trading at multi-month lows on the last day of 2021, reaching a low of -1.13%, an indication that markets viewed the future prospects for the economy as bleak and discouraging, indicative of chronic disbelief in the Fed's ability to raise rates decisively: in the first week of 2022, real rates have soared to -0.8%, the highest level since June.

The result has been a sharp upward movement in nominal rates, which, as we mentioned, are trading at 1.75%, exceeding last year's high in March 2021 and the highest level since pre-COVID, because the fall in breakevens has been more than offset by the rebound in real rates.

Clearly, this higher (less negative) movement in real terms is in response to market confidence that US economic growth can withstand a faster monetary normalization process, but it could also begin to put pressure on market valuations (multiple compression), especially considering that, compared to the post-financial crisis normalization cycle, real rates remain at extremely depressed levels.

We believe that the risks of corrections have been increasing, which in any case could provide better entry points for 2022, given that from current levels the upside for equities seems limited and valuations somewhat stretched, which is particularly true for the US market and even more so in the large technology sector.

Our recommendation? Stay away from growth sectors, at least for the first part of the year, favor short-duration value investments (which are therefore less sensitive to interest rate hikes) and position yourself for a steeper curve (financial sector, energy), diversify outside the US into developed markets where valuations are more attractive (Europe and Japan), and maintain a very conservative strategy in terms of duration in international fixed income.

Finally, consider maintaining some liquidity (to seek better entry points) for the rest of the year.

Humberto Mora, Strategy and Investments