Last week, we recommended increasing exposure to commodities, as the escalating geopolitical tensions have significantly heightened the risk of further exacerbating the energy and commodities crisis that has unfolded over the past two years. Potential disruptions to trade in oil, gas, grains, and metals now pose a significant risk to investments and the real economy. Investors should, therefore, hedge against this risk by increasing their allocations to commodities, energy, and materials. These allocations would serve as a hedge against inflation and geopolitical risks.

Well, this week we want to reaffirm our view on the benefits of adding commodities to a portfolio in the current environment and delve deeper into this investment thesis.From a strategic perspective, commodities not only serve as a hedge against geopolitical risks, but also as a hedge against inflation and against valuation risk stemming from changes in central banks’ policy responses.

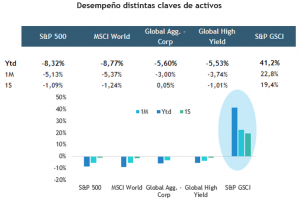

And the case for diversification has rarely been stronger, with commodities up 40% year-to-date—half of that gain occurring over the past week (as measured by the S&P GSCI Commodity Index)—and stocks down 8% (as measured by the S&P 500).

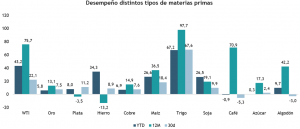

The case for investing in commodities has rarely been stronger, and the growing geopolitical tensions surrounding Ukraine have only heightened the focus on commodities. While the market is still operating under a base-case scenario of a limited disruption to food and energy flows (assuming that none of the governments’ economic interests involve using food or fuel as a lever against Russia), nearly all major commodity markets are in a state of severe strain and are therefore highly vulnerable to even the smallest shocks. Furthermore, each disruption increases the likelihood of another crisis, with shortages in one market triggering insolvency in another—as has been seen, for example, in the European gas and aluminum markets.

While many commodities are fundamentally exposed to events in Ukraine, it is oil and gold that provide the cleanest hedges against this geopolitical risk. First, there is a clear upward bias in oil prices, from both a tactical and strategic perspective, with any geopolitical risk premium coming on top of the tightest inventory levels in decades, low spare capacity, and a much less elastic shale sector. According to Goldman Sachs estimates, if the oil market is forced to rebalance by 2022—one year earlier than its base-case price of US$105/bbl—the price of oil will have to reach US$125/bbl to achieve near-complete rebalancing through the destruction of demand. The key catalyst for a bullish oil outlook would be an agreement with Iran; however, the geopolitical obstacles to this appear to be stubbornly high.

Along the same lines, it is clear that as geopolitical tensions rise, gold is acting as a currency of last resort, since gold tends to react to geopolitical risks that could directly affect the U.S. Thus, the current energy crisis and U.S. inflation above target mean that any disruption in the flow of raw materials from Russia could fuel greater concerns about excessive U.S. inflation and a subsequent hard landing.

Currently, in our sector strategies, we are recommending exposure to commodities through two channels

– In the U.S. energy sector through the SPDR Energy Select Sector ETF (XLE).

– In the mining sector, through the iShares MSCI Global Metals & Mining Producers ETF (PICK).

– Are you looking for a more direct way to gain exposure to commodities? A good option is the iShares S&P GSCI Commodity-Indexed Trust (GSG) ETF, which has, among its largest holdings, 60% in energy, 18% in agriculture, 11% in industrial metals, and 4% in precious metals.

– For direct exposure to gold, one option is the SPDR Gold Shares ETF (GLD).