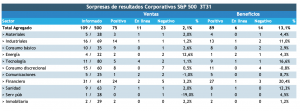

We are approaching the busiest part of the third-quarter earnings season, with nearly 50% of U.S. companies scheduled to report next week. So far, only 21% of U.S. companies have reported. While it may still seem too early to make a meaningful assessment, initial results point to better-than-expected earnings growth, with third-quarter EPS growth of +44% year-over-year, and it is encouraging that the combined third-quarter EPS for the S&P 500 is beginning to trend higher.

86% of S&P 500 companies that have reported have beaten EPS estimates. EPS growth for these companies is +44% year-over-year, with a positive surprise of 13%. Materials and Discretionary are posting the highest growth among sectors, although very few companies have reported to date in either sector. Top-line growth is reaching +16% year-over-year, beating expectations by 2%.

On the top line, 69% of companies are beating sales estimates. Overall revenue growth is +16% year-over-year. All sectors, excluding utilities, are experiencing positive revenue growth.

The S&P 500's combined EPS for Q3 2021 has risen to US$50 (+29% year-over-year), compared with +14% year-over-year at the beginning of the year.

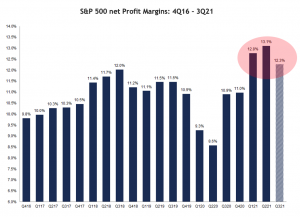

Another point worth noting, given market concerns about rising inflation, is that the S&P 500 is reporting its third-highest net profit margin since 2008 for the third quarter, and it is above both the net profit margin from the previous year and the five-year average of 10.9%.

We believe that these earnings trends do not in any way reflect concerns about a slowdown in economic growth, and that higher inflation is currently being absorbed well.

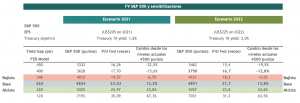

Finally, we expect the third-quarter earnings season to support risk assets over the coming weeks and beyond. Buying the dips has continued to be an effective strategy, and now that we are on the verge of breaking through all-time highs, we believe targets in the 4,800–5,000 range for the S&P 500 represent the most likely path.

Furthermore, financial conditions remain highly accommodative and will continue to do so despite an expected tightening of monetary policy. Inflationary pressures are forcing central banks to move away from ultra-accommodative policies, not only because inflation has risen uncomfortably above their targets, but also because inflation depresses real policy rates, making current monetary policy even more accommodative than the nominal policy rate suggests.

However, as long as real yields remain subdued, they should not put significant pressure on market valuations, which, in any case, remain quite favorable relative to interest rate levels.

Humberto Mora

Strategy and Investments