The FOMC left the target range for the federal funds rate unchanged at 0–0.25%. The Committee acknowledged that the test of “substantial further progress” for tapering has been met and announced that it will begin reducing monthly increases in its holdings of agency MBS and Treasuries starting in mid-November. The Committee specified a reduction of US$15 billion in asset purchases in November and December (US$10 billion in Treasuries and US$5 billion in agency MBS holdings), and considered that the pace of US$15 billion per month "would likely be appropriate," but that it is "prepared to adjust the pace of purchases if changes in the economic outlook warrant it." Assuming the FOMC does not pause or change the pace of reduction, the final reduction would be announced at the May 2022 FOMC meeting and the last one would be implemented in mid-June 2022, probably a couple of days before the June meeting.

The characterization of the current economic situation continued to emphasize the impact of COVID-19 on economic activity, but was updated to acknowledge that virus cases have slowed since the summer.

Inflation was again characterized as "elevated," but the assessment "largely reflecting transitory factors" was diluted to "largely reflecting factors that are expected to be transitory," and the statement noted that pandemic-specific supply and demand imbalances and reopening effects have contributed to higher prices.

In addition, the Committee updated the statement to acknowledge that "easing supply constraints, as well as progress on vaccines, are expected to support" continued economic gains and a reduction in inflation, but that risks to the outlook "remain."

The question that follows is : Why has the much-feared "tapering" not generated greater volatility in assets, and why are we ending another record week in equities?

A few weeks ago, we pointed out that investors should bear in mind that the Fed is moving forward because it has more confidence in the economy and will continue to provide support. While higher bond yields reduce the relative attractiveness of stocks, a gradual increase in bond yields should be more than offset by the positive impact of rising corporate earnings as economies return to normal. Therefore, the Fed's tapering should be viewed as the gradual withdrawal of an emergency support measure as conditions normalize.

In this regard, we believe it is essential to continue distinguishing between asset purchase tapering and rate hikes. Today, real interest rates remain extremely expansionary, especially considering the "greater tolerance" for higher inflation, which makes the Fed's current monetary policy even more accommodative than the nominal policy rate suggests.

In our base case scenario, we will continue to see higher inflation, but also higher growth (something reaffirmed in this week's Fed statement). In this regard, we believe that the correct approach is to continue overweighting equities over fixed income, where relative valuations continue to offer a large premium for their history and equities are the only asset class that produces positive real returns and tends to perform well in a higher inflation environment.

We also highlight:

Economic data is improving. The week ends with strong job creation figures in the US (531,000 jobs were created, well above the consensus estimate of 450,000), a report that is more consistent with what is happening in an economy that remains solid and is growing well.

The Q3 2021 corporate earnings season has ended with solid results, with 81% of S&P 500 companies reporting earnings per share (EPS) above estimates. EPS growth for these companies stands at +41% year-on-year, which is a positive surprise of 10% , and the outlook remains favorable. (The proportion of companies revising their EPS guidance upward is approaching decade highs.)

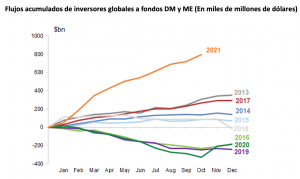

Equity inflows remain strong. Equity inflows this week totaled US$26.1 billion and have already exceeded US$800 billion in 2021.

Humberto Mora

Fynsa Strategy and Investments