Since September 14, the nominal yield on 10-year U.S. Treasury bonds has risen by 26 basis points (from 1.28% to 1.55%), and the real yield on 10-year U.S. Treasury bonds has risen by 20 basis points (from -1.05% to -0.85%).

That said, interest rate movements so far have been less drastic than in early 2021, but the economic environment is less favorable for stocks at present. In general, stocks have struggled when higher real rates were driven by perceived shifts in Fed policy (e.g., the “taper tantrum” in 2013, “long way from neutral” in 2018) and have performed better during periods of improving growth (for example, after the 2016 election and the passage of tax reform in late 2017). The real yield on 10-year U.S. Treasury bonds rose by 50 basis points between late February and mid-March, a move of approximately 3 standard deviations. However, that move largely reflected the continued improvement in the economic growth outlook following the vaccine announcements in early November. Today, economic growth is slowing, and the Fed is expected to announce the start of tapering at its November meeting.

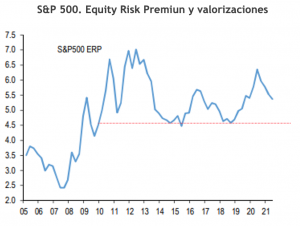

So the next question is … Is an aggressive Fed a problem for the stock markets?One transmission channel through which a more aggressive Fed could hurt stocks is via a rise in real rates, as higher real yields reduce the relative valuation advantage of stocks over bonds. However, we still find it difficult to characterize stocks as expensive when real yields remain so negative, with the 10-year real UST at -88 bp. This level of real yields implies an equity risk premium of around 5.3% currently for the S&P 500. During the previous corrections in 2015 and 2018, the equity risk premium bottomed out at 4.5%. Therefore, strictly speaking, we would need to see the 10-year real yield rise by 80 basis points from current levels for equity risk premiums to fall to 4.5%.

We continue to believe that the pace and direction of interest rate movements will be more important for stocks in the short term than the level of interest rates itself.Stocks remain attractively valued relative to interest rate levels. Using a P/E multiple of 20x and a 10-year UST yield of 1.5%, the earnings yield spread between stocks (4.9%) and bonds is 345 basis points, placing it at only the 39th percentile historically. Assuming no change in the P/E ratio, the 10-year UST yield would need to rise above 2.3% for relative equity valuations to move above their long-term average.

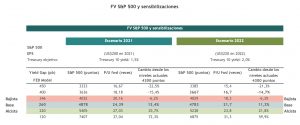

With these variables, we are in a position to project the future potential of equities. Barring any major negative surprises, we believe that the fair value range for the S&P 500 would be between 11% and 13% from current levels, with downside risk limited to 6% (which we assign a low probability of occurrence); therefore, the recent pullbacks would still qualify as “Buy the Dips.”

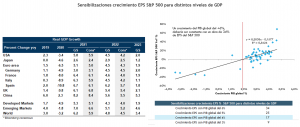

Our baseline scenario assumes that base rates will end the year around current levels (with some upside risk), although for 2022 we must begin to factor in higher interest rates amid rising inflationary pressures—and also because we expect global growth to pick up again.

For now, we prefer to take a conservative approach to earnings estimates for 2022, with an expected EPS of US$220 (+10%) for the S&P 500 (in line with market consensus), although we preliminarily believe there is upside risk, given that growth expectations for 2022—both globally and in the U.S. itself—are likely to remain above potential; barring runaway inflation, earnings growth could very well exceed expectations.