After a stellar 2020, investments in renewable energy have become more volatile and are trading well below the broader market.

Several factors account for this trend, including geopolitical tensions, concerns about supply chain-induced shortages, uncertainty surrounding Biden's fiscal plan, and some pressure on valuations due to rising interest rates.

- Of all these factors, supply chain disruptions and geopolitics remain a key concern for investors in the short term. The impact of supply chain disruptions varies greatly by company and market. However, studies suggest that most existing utility-scale projects are still underway, while some new project decisions are being made in fiscal year 2022. In the residential market, price increases are being passed on to customers, and demand remains strong.

- Demand remains strong in the U.S. residential market, although some new utility-scale projects may be delayed due to cost increases and logistical challenges. Existing utility-scale projects appear to be on track.

- Supply chain challenges appear to be stable, not worsening.Shipping and logistics remain the common headwind across the industry. For now, solar panels are allowed into the U.S., with the exception of one Chinese supplier, and large installers appear to be able to meet demand for new shipments, in addition to the visibility provided by strategically high inventory levels.

An industry with great potential

The U.S. Department of Energy recently published a study on solar futures (Solar Futures Study | Department of Energy), assessing the potential role of solar energy in decarbonization. The study includes a baseline scenario that generally aligns with BNEF (Bloomberg New Energy Finance) forecasts and estimates that emissions from the energy sector will decrease by 45% from 2005 levels by 2035. However, two other “decarbonization” scenarios—which assume that emissions from the energy sector will decrease by 95% from 2005 levels by 2035—indicate that solar installations will need to account for up to 40% of the electricity supply by 2035, compared to the current ~4%. These decarbonization scenarios would require solar capacity to grow by an average of 30 GW annually through 2025 and increase to 60 GW annually between 2025 and 2030 (installations in 2020 totaled ~19 GW). We believe these studies could prove critical to policy decisions regarding the potential U.S. budget reconciliation bill, as well as to U.S. commitments for the upcoming United Nations COP26 conference in November.

Possible positive catalysts on the horizon

- In addition to company-specific catalysts (with Q3 2021 corporate results from the sector’s leading companies far exceeding estimates), investors are closely focused on potential positive catalysts for the industry as a whole—primarily government regulations and incentives—which could make the strong secular tailwinds even more favorable. We believe that governments could present more detailed plans—including short- and medium-term targets—for the long-term decarbonization goals that have already been outlined for the United Nations COP26 meeting in early November.

- In a recent study by J.P. Morgan, market participants appear optimistic about the potential for additional government incentives, whether as part of the budget reconciliation bill or otherwise.The extension and expansion of the ITC to include off-grid storage, as well as the direct payment option, are seen as key drivers of industry growth. There is also some optimism that incentives for domestic manufacturing could be introduced, which would be less detrimental to the U.S. government’s climate change goals while also diversifying the global supply chain. That said, uncertainty persists regarding the possible expansion of import restrictions, as well as the possible expansion of anti-dumping and countervailing duties on panels manufactured in Southeast Asia.

Biden's Fiscal Plan

Although the market has become more skeptical that the U.S. budget reconciliation bill will be passed in its current form, the portion related to clean energy is not at risk.

Furthermore, we note that many major companies in the sector are trading at a discount to the average multiple immediately prior to the 2020 U.S. elections, so even the passage of a scaled-back version of the bill would likely be viewed favorably.

Biden's new fiscal plan allocates $555 billion for clean energy, with a focus on incentives.

- The spending would represent the largest climate investment in U.S. history.

- The spending is aimed at technologies to reduce emissions in buildings, transportation, industry, electricity, and agriculture.

- The initiatives will begin to reduce pollution immediately, with more than one gigatonne of greenhouse gas emissions cut by 2030, according to the plan’s framework. This will put the U.S. on track to reduce emissions by 50% to 52% below 2005 levels by 2030.

- The plan includes a 10-year expansion of tax credits for residential and utility-scale clean energy, transmission, storage, electric vehicles, and clean energy manufacturing. More than US$100 billion is set aside for investments in resilience as extreme weather events—including wildfires fueled by climate change—plague the U.S.

- The plan also aims to boost domestic manufacturing in the clean energy sector. Biden has said this will create hundreds of thousands of new jobs.

Some Market Insights and Investment Opportunities

- To some, certain market trends may seem contradictory. Over the past 12 months, gas prices have risen by 450%, coal prices have nearly quadrupled, and, as a result, energy futures prices have more than doubled. This has led to a 35% to 50% increase in energy bills for end users across Europe (where the impact of rising gas prices is felt most acutely).

- Many of these trends are linked to supply issues, a lack of visibility regarding investments in traditional energy sectors, and stronger demand as pandemic-related restrictions begin to ease. However, we believe this should also accelerate decision-making to promote low-cost clean energy.

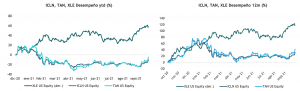

- So far this year, amid rising oil prices, the U.S. energy sector has returned 58%, while renewable energy indices such as the ICLN (SHARES GLOBAL CLEAN ENERGY ETF) and the TAN (INVESCO SOLAR ETF), which tracks solar companies, have fallen 10% and 5%, respectively. Over a 12-month period, the differences persist: while the XLE energy sector has returned 119%, the renewable energy indices ICLN and TAN have returned only 32% and 42%, respectively, which, incidentally, is a very good performance, but it is striking how far behind they lag compared to traditional energy sources.

- That said, things have started to change in October, driven in part by positive corporate earnings reports over the past week. So far in October, the clean energy ETF (ICLN) has returned 15.5% over 30 days, while the benchmark for solar companies (TAN) has returned +22.5% over the same period. This compares favorably to the +9.38% return for the traditional energy sector (XLE) and the broader market’s +5.7% return (S&P 500).

- Otherwise, investors seem to be returning more decisively to the renewable energy sectors, as evidenced by the strong issuance of shares in sector ETFs in recent weeks.

- Finally, we believe there are more gains ahead and see significant potential in clean energy, which is well worth including in an international equity portfolio with a long-term outlook, or as a tactical opportunity for trading-oriented investors.

Decline in investment

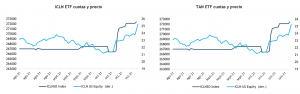

- iShares Global Clean Energy ETF (ICLN)

Humberto Mora

Strategy and Investments