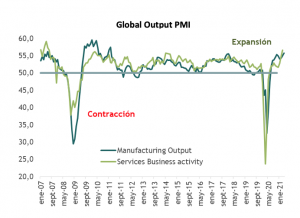

The rebound in economic growth since the slowdown at the turn of the year continued to gain momentum at the start of the current quarter. Immediately following a 1.6-point jump in March, JP Morgan's global PMI strengthened by another 1.5 points in April and now stands at nearly a 14-year high. The recovery is even more remarkable given that the survey barely registered a setback during the second wave of the pandemic.

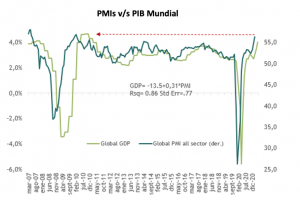

At 56.3, the composite reading in the global PMI for the entire industry is consistent with growth of almost 4% in global GDP. While this is below estimates for 6% growth in global GDP this quarter, it is typical for PMIs not to capture extremes. Given that global GDP in the coming quarter is expected to expand at one of its fastest rates in decades, it should come as no surprise that PMIs are underperforming. Rather, the message from the PMIs is twofold: 1) the rapid increase is consistent with a sharp acceleration in activity, and 2) the nearly 14-year high is consistent with booming growth.

Equally encouraging in the April report are signs that the global services sector is coming back to life. The global pandemic recession of 2020 was unique both for its impact on services sector activity and for the depth of the recession. As a result, the global services PMI spent 13 months below the manufacturing PMI. This underperformance ended in April, with the services PMI rising by almost 2 points to 56.6, almost a point above the manufacturing PMI, which also advanced by 0.9 points.

Although the April survey shows significant breadth of strength across all sectors and components, this is partly offset by stronger gains in the US and UK compared to more modest, albeit still solid, gains elsewhere. Both the US and UK have made considerable progress with vaccinations in recent months. At the same time, increased fiscal stimulus in the US is adding further fuel to its boom through the second wave. Elsewhere, the recovery has slowed more markedly. These regional divergences should close in the coming months with increased normalization in Europe and catch-up growth in the rest of the world.

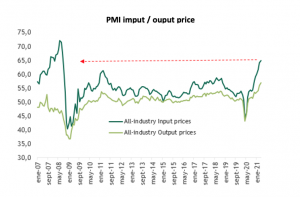

With economic activity accelerating sharply, bottleneck pressures related to disruptions in some supply chains are evident in price PMIs. In recent months, there has been a significant increase in the price of PMI inputs, and these pressures could eventually spread to overall consumer price inflation.