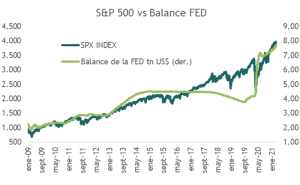

Market performance trends and the Fed’s balance sheet are strongly correlated. Total assets on the Fed’s balance sheet have expanded from US$2.24 trillion at the end of 2008 to the current level of around US$7.7 trillion, representing 244% growth, while the S&P 500 rose from 903.25 to approximately 3,900 points, posting cumulative growth of about 330% over the same period. (See Figure 1.)

It’s true, the numbers aren’t exactly the same, but look at what has happened during the pandemic, when earnings have fallen and the entire return on equities is attributable to the expansion of multiples. The Fed’s balance sheet has increased from $4.67 trillion on March 18, 2020 (one week before the market bottom) to $7.7 trillion, a 65% increase, while the S&P 500 has risen 64% over the same period. That does look similar, doesn’t it?

Since mid-February of this year, equity markets have struggled to sustain their upward trend amid a rapid rise in sovereign yields that has put high market valuations to the test, but also amid reduced liquidity provided by major central banks. (See Chart 2)

It’s not that asset purchases have stopped (G-10 central banks are expected to purchase nearly US$300 trillion per month in 2021), but the pace of these purchases has slowed. How long will this last? Not very long, as central banks have become increasingly sensitive to changes in liquidity and how they impact prices.

Here are three examples:

The European Central Bank (ECB) stated two weeks ago that it will buy more debt so that rising interest rates do not stifle the recovery, and it’s not that the size of the purchase program has increased (at least not for now), but rather that the pace of purchases will accelerate.

Chinese stocks have struggled this year, due to regulatory issues, but also because of growing expectations of a more restrictive monetary policy. China hasn’t been this conservative in its cash injections to banks in nearly a year, and the People’s Bank of China has avoided net short-term liquidity injections into the financial system since late last month, raising concerns that access to funds is becoming increasingly difficult. How long will this last? After a 15% drop in Chinese stocks since mid-February, probably not much longer.

Japanese stocks have seen a broad sell-off in recent days, after the Bank of Japan (BOJ) indicated last week that it is phasing out its annual stock-purchase target. And surprise!! The BOJ had to return to the market more aggressively to buy a record amount of stocks (70 bn) and halt the decline (which it has managed to do so far).