Today, there are two proposals from the opposition to:

Although both bills could be rejected by the Constitutional Court, the fact is that they have been gaining momentum, thanks to support from multilateral organizations for increasing tax revenue to address the pandemic’s impact on public spending, and because the third 10% withdrawal from pension funds (AFPs) has already been approved by the Chamber of Deputies by a large majority and is now moving to the Senate, which is expected to debate and vote on it next week.

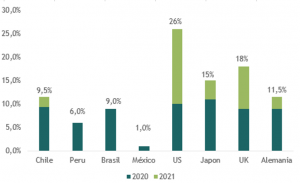

Chile has implemented a robust fiscal response, placing it at the forefront of both the region’s economies and emerging markets worldwide. (see chart)

Whether or not the third withdrawal from pension funds—or other alternatives currently on the table, such as withdrawals from unemployment insurance funds—is ultimately approved, and with lockdowns being extended for longer periods, it is likely that the government will have to make an even greater fiscal effort in any case, thereby strengthening an already abundant liquidity environment.

What is the practical effect of this increased liquidity on local assets, at least in the short term?

Overall, it is good for consumer spending (positive for retail companies); it may continue to improve asset quality as people use their excess liquidity to pay down their debts (positive for banks) ; and it has the potential to drive higher inflation (positive for funds denominated in UF).

In the long term, if the additional liquidity comes from another withdrawal from the AFPs, it could be interpreted as an indirect increase in government debt, which could continue to put pressure on long-term market rates.

Fiscal Stimulus 2020–2021 (% of GDP)

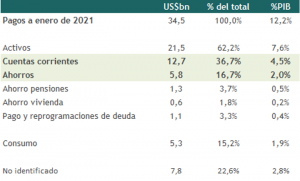

US$12.7 billion in liquidity in consumers' checking accounts (4.5% of GDP)