Building portfolios capable of generating attractive returns for investors with acceptable levels of risk is likely facing its most challenging period yet, given the context of low fixed-income rates and high stock valuations, coupled with the prospect of rising inflation. That is why the traditional bond/stock mix—which has worked quite well over the past 40 years—needs to be reconsidered, and new asset allocation models need to be implemented.

Among the most promising opportunities available are “Core” alternative asset classes, which offer low volatility and attractive diversification benefits. An asset class is considered “Core” if a large percentage of its total return comes from cash income and its cash flows can be forecasted over long periods of time with a low margin of error. Examples of this include senior secured loans or real estate assets.

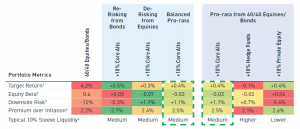

Just 10% of the portfolio allocated to “Core” Alternative Assets can significantly improve portfolio returns, whether by shifting that allocation to bonds, stocks, or a balanced mix of both. For example, the expected annual return can be increased by +0.5% by shifting allocation from bonds to “Core” Alternatives, while downside risk can be reduced by 1.9% by replacing stocks with these asset classes.

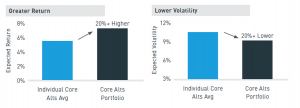

Cross-correlations within the “Core” Alternative Assets universe result from fundamentally different return drivers for each asset class. All components of a portfolio must be selected in such a way that there is a low correlation between each component, thereby delivering higher returns with lower volatility than if a portfolio consisting of only one class of Alternative Assets were chosen, as can be seen in the following charts.

Allocating 10% of the portfolio to alternative assets—while offering lower liquidity—falls within the liquidity tolerance accepted by most investors, especially in an environment where the public market is expected to yield unacceptably low rates.

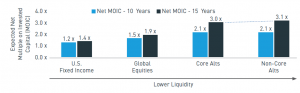

Expanding on the above, when examining the spectrum of less liquid assets, “Core” Alternatives exhibit a somewhat hybrid liquidity profile, with relatively short lock-up periods and higher cash flows than those available in some segments of the private markets. Since many investors will not need immediate access to the income stream, reinvesting the income within “Core” Alternatives can generate net return multiples equivalent to those of less liquid strategies such as private equity.

Investors’ portfolios continue to consist of stocks and bonds, despite well-founded concerns that it will not be possible to achieve levels of return and risk consistent with historical experience. In this context, investors need solutions that can enhance returns without adding risk. “Core” alternative assets are a solution just around the corner that can generate stable returns above those of public markets, while providing attractive protection against downside risks along with resilience in the face of inflation and rising interest rates.

Source: Preqin and JP Morgan Asset Management.