The Biden administration unveiled a plan that would raise corporate taxes to fund its proposed $2.3 trillion infrastructure package.

In particular, discussions about a global minimum corporate tax rate have gained new momentum after U.S. Treasury Secretary Janet Yellen raised the issue in a speech earlier this week, citing the need to avoid a “race to the bottom.”

The main motivation behind this initiative would be to prevent or discourage companies from shifting their profits or their domicile to tax havens, as well as to put an end to “tax competition” between regions.

The establishment of a minimum corporate tax rate to discourage companies from filing taxes in countries with the lowest rates has been a key pillar of the OECD's discussions, but reaching an agreement would not be easy:

But discussions about taxes are not limited to permanent changes. This week, the International Monetary Fund proposed a temporary “solidarity” tax on those who have profited from the pandemic and the wealthiest individuals. High-income individuals and companies that thrived during the coronavirus crisis should pay additional taxes to show solidarity with those hardest hit by the pandemic, according to the IMF.

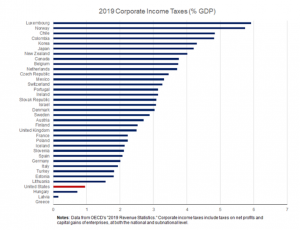

Corporate tax revenue in OECD countries as a percentage of GDP

Over the past two decades, the typical OECD country has raised about 3 percent of GDP in corporate taxes. And while the United States has historically raised comparatively less revenue through corporate taxes than its trading partners, the gap was greatly exacerbated by the 2017 tax law. In fact, closing even half the gap between the U.S. corporate tax burden and the median OECD tax burden is roughly enough to pay for the initiatives proposed in the American Jobs Plan.