Beyond the evident slowdown in the global economy in recent months, as a result of the resurgence of COVID-19, we believe this should be adequately offset by greater policy support, especially in China, which would shift from a tight monetary stance to a more accommodative one—whether by easing monetary policy or implementing some form of more targeted fiscal stimulus—or by the Federal Reserve delaying any announcement of a tapering of asset purchases until December, which remains our base-case scenario.

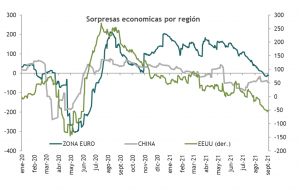

That said, we have always maintained that this post-COVID recovery would not be without challenges, that it would be uneven across regions, and that it would ultimately take the form of a “staggered recovery”, since different regions were affected by COVID-19 at different times. China was the first to enter the crisis and the first to emerge from it, while the U.S. recovered later (peak quarterly GDP growth occurred in Q2 2021), followed by Europe (peak quarterly GDP growth in Q3 2021) and, finally, emerging markets excluding China—all in tandem with the easing of COVID-19 mobility restrictions.

These varying recovery timelines help explain very well how assets have performed in different regions, with an exceptionally strong United States, which has been the driving force behind global equities for much of the year, and now we’re seeing Europe catching up. Are emerging markets next in line? As vaccination rates rise and economies reopen, emerging markets are expected to regain their GDP growth premium relative to U.S. GDP by Q4 2021 and thus resume outperforming in the equity markets.

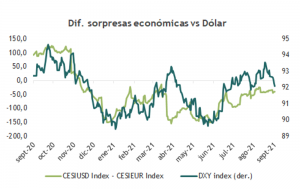

But let’s get to the reason we’re here today. These same economic divergences allow us to explain the behavior of the foreign exchange market quite well. A stronger U.S. economy and expectations of an early normalization by the Fed have led to a stronger dollar, causing the market to drastically scale back its original expectations of a weaker dollar in 2021.

Well, we still haven’t abandoned our view that the dollar will weaken further, and recent events give us enough confidence to stick to that so-called. While economic data has been disappointing in most regions, the U.S. is where this has been most evident after China (just look at this week’s disappointing employment data and the substantial drop in consumer confidence, to name a few).

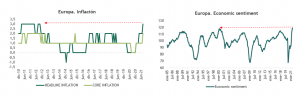

But if we look at Europe, the loss of momentum has been more moderate, and it has been accompanied by a significant factor: higher inflation, which has even led to calls within the ECB for an early withdrawal of stimulus measures. We do not believe this will happen because Europe still has a long way to go to recover its pre-pandemic levels of economic activity and has considerably more room to maneuver than the U.S., especially in the labor market, but we do believe that Europe’s stronger momentum (compared to the U.S.) could significantly reduce the dollar’s relative appeal.

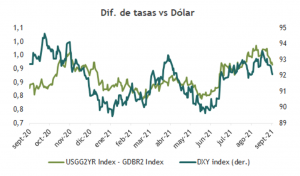

In practice, both interest rate differentials and economic surprise differentials have been shifting in favor of the euro (a weaker dollar), a trend we expect to intensify in the coming weeks, especially if the Fed maintains a rather cautious tone in September.

If this is correct, expect better relative performance from non-U.S. assets and higher commodity prices (due to the denomination effect).