On Thursday, European Central Bank policymakers convened for their first monetary policy meeting after abandoning their long-standing inflation target of “below, but close to 2%” in favor of a new symmetric target centered on 2%. That decision formalized the ECB’s shift away from its Bundesbank-style approach to price stability and cemented its role as the eurozone’s “guardian of financial stability.” However, ahead of Thursday’s meeting, investors still needed to know for certain how the ECB’s strategy shift would affect (i) the outlook for eurozone interest rates and (ii) the future of the ECB’s bond purchases.These questions have now been answered.

As for interest rates, the ECB was unequivocal and emphatically dovish. There was never any doubt that the Governing Council would signal that rates would remain at record lows for an extended period. But comparing the ECB’s new forward guidance with historical data underscores how unlikely any rate hikes are in the medium term. The ECB expects interest rates to remain at their current levels or lower until three conditions are met.

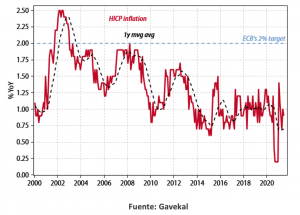

This raises the bar for future rate hikes.In the past, the ECB’s forecasts sometimes projected core inflation converging toward 2% over the medium term—for example, in June 2018 (which was one of the factors behind the ECB’s decision to halt net asset purchases at the end of 2018). But actual core inflation did not meet the ECB’s forecasts. As the accompanying chart shows, the last time core inflation in the eurozone reached 2% was in March 2008. The one-year moving average of core inflation has not risen above 1.2% since 2013. Combined with the first two conditions, this virtually guarantees that there would be no rate hikes until at least 2024.

The ECB did not directly address the future of its asset purchases on Thursday. Currently, most of its net purchases are made under its Pandemic Emergency Purchase Program (PEPP), which costs about 80 billion euros per month, compared with a limit of 20 billion euros per month for its regular asset purchase program (APP). Since the PEPP is set to expire in March 2022, the ECB will have to either extend the PEPP or increase the size of the APP if it wants to avoid market destabilization by abruptly reducing its net asset purchases by 80bn euros per month.

Indirectly, the ECB’s future guidance on interest rates has implications for the future of its asset purchases. The ECB has said it expects to end net asset purchases shortly before raising rates (although it will continue to roll over bonds that mature after that). As a result, the ECB’s commitment on Thursday to keep interest rates low for longer also amounts to a commitment to continue its net purchases in the bond market for longer.

Core inflation in the eurozone has not exceeded 2% since early 2000