When we started this column, the idea was to explain in simple terms some economic phenomena related to the current situation, everyday life, or even some that people might not necessarily identify as “economic” per se. We did some of that, but as you can understand, a series of recent events has led us to shift our focus to issues related to the profound national debate we are currently engaged in.

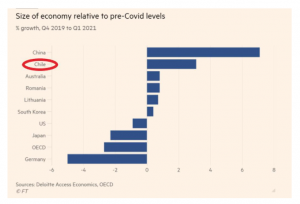

However, a post that began circulating on social media and in emails within the financial sector caught my attention. Not only because of its bold title, but also because the source seemed reputable and reliable to me. It’s a chart that supposedly shows the countries that have left the aftermath of the pandemic behind and now have larger economies than they did before the COVID-19 pandemic. Of course, it also included those that are still lagging behind in this regard. But see for yourselves:

Thus, we observe that the economies of China, Chile, Australia, Romania, Lithuania, and South Korea would be larger relative to what they were before the pandemic. Methodologically, it compares GDP for the first quarter of 2021 to that of the fourth quarter of 2019 for a set of countries. If the change is positive, the economy is larger; if it is negative, the opposite is true. When attempting to replicate this analysis for Chile, we note that it was based on the seasonally adjusted GDP series and was not annualized. Thus, the result obtained is 3.1%.

I have several concerns in this regard. The first has to do with the concept of “size of the economy.” Clearly, the authors consider this to be a flow (GDP, by definition, is one), whereas for me it would be a stock. Call me a (neo)classical economist, but for me, the size of the economy at a given moment is the result of some production function that depends on the stock of physical capital, human labor, and productivity. A stock.

“Yeah, but Nathan, that’s so boring—let’s not reduce the problem to a semantic issue. Give us something more interesting than that.”. Yeah, you’re right. Let’s ASSUME for a moment that the size of the economy is GDP (*my eye twitches*). And that seasonally adjusting the data is enough to make GDP figures from different quarters somewhat comparable (ugh!). In an effort to standardize the data, the author chose the fourth quarter since, for most countries, it was still a normal quarter. But we know that for Chile, it was anything but normal. During this quarter, economic activity contracted by 2% year-over-year (4% if we exclude December) following the social unrest, which significantly lowers the basis for comparison. Stretching the methodology a bit, when looking at monthly data (using the seasonally adjusted Imacec), we conclude that as of April, the economy was 3.1% smaller than in September 2019, as shown in the following graph:

This figure shows that the monthly production level in April 2021 is 3.1% lower than it was in September 2019, after adjusting for seasonal effects. Therefore, upon closer examination, we realize that we have not yet reached pre-crisis levels.

But that’s not the whole story. The chart above highlights an ellipse that shows the decline in output levels during the two crises. This can be quantified; we can determine how much output we lost between the fourth quarter of 2019 and the first quarter of 2021. To do so, I’ll make a conservative assumption: that during that period we would have grown at the same rate as the average over the past 80 months—2.4% annually (or 0.2% seasonally adjusted month-over-month). Based on that, during this period, we lost approximately US$28 billion in output. If we want the economy to fully recover from this recessionary phase, it is not enough simply to return to our previous level; we must also recoup that loss. If we settle for returning to our previous growth rate, we will be US$28 billion poorer forever. And in a context where social demands are pressing, that is not a luxury we can afford.

So, friends, when you see any kind of chart or information like this, be skeptical. Allow yourselves to be skeptical. Feel free to doubt even this column I’ve written, if I haven’t managed to convince you. Not because of my title or my position, or because I’m a “Big Four” firm. Judge our ideas and arguments—that’s the only way we’ll move forward. For now, bakers, stick to your cakes.

Nathan Pincheira

Chief Economist at Fynsa