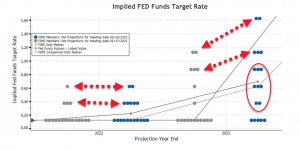

The Fed kept its benchmark rates and the pace of bond purchases unchanged, but the biggest change is a more hawkish shift in its rate forecasts, as the Fed’s median projections call for two rate hikes by the end of 2023 and seven FOMC members expect a hike in 2022.

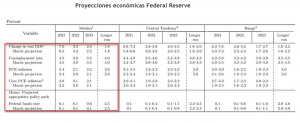

On the economic front, the biggest revision is to this year’s inflation forecast, which they continue to characterize as “transitory.” There were no signs of higher unemployment in 2023, which remained unchanged from the previous projection. What did change was a slight increase in 2023 GDP, from 2.2% in March to 2.4%, while PCE inflation also rose from 2.1% to 2.2%, giving the Fed some leeway to forecast two rate hikes in 2023.

Fed Chair Jerome Powell sees no reason to reverse course and begin aggressively tightening policy, and he reiterated his view that (i) much of the current inflation is due to transitory factors, (ii) inflation expectations are above target, but still within an acceptable range given the Fed’s willingness to keep inflation moderately high for a while, and (iii) the U.S. labor market has some slack.

We believe the Fed had to signal higher interest rates in response to the higher-than-expected inflation figures, but that it should extend its asset purchases as long as possible, and that the market is much “more sensitive to liquidity” (see attached charts) than to a slight increase in the TPM. Moreover, there is still a great deal of debt left to “monetize.”

The tug-of-war between above-trend growth and policy normalization is what will determine the direction of the markets in 2H21 and beyond… And although the Fed was somewhat more aggressive than expected, growth is likely to continue setting the tone over the coming months. This global dichotomy favors equities, emerging markets, value stocks, commodities, and cyclical stocks. We see the reflation and reopening that took place in the U.S. spreading to Europe and beginning in emerging markets.