In previous issues, we have argued that the impact of changing inflation on stocks depends on the initial level of inflation and the direction of the trend.

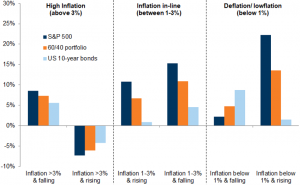

The combination that tends to be most favorable for stock markets is when inflation is rising from very low levels (and the risks of deflation are receding) or when high inflation rates are moderating. As the chart shows, for stocks, bonds, and balanced funds, higher inflation (above, say, 3%) that is rising tends to be the worst outcome, while inflation above 3% that is falling is much more benign. For stocks in particular, the best returns tend to occur when inflation is below 1% but rising; this is often associated with a recovery from a recession and also with a declining risk of deflation (and, therefore, is not particularly favorable for bond markets).

Stable yields with inflation within the range: the reversal of extremes tends to be bullish

However, as we showed earlier with regard to the PMIs, there has been a significant increase in input prices as measured by the PMI in recent months, and these pressures could eventually spill over into overall consumer price inflation. We should also note that many companies that have reported their Q1 2021 results have mentioned inflationary pressures.

So the next question is: What would happen if we moved from “higher temporary inflation” (base case) to “higher persistent inflation”—say, around 3% (risk scenario)?

First, you should further shorten the duration of your portfolio and reallocate from bonds to commodities and stocks. Commodity indices (such as the S&P GSCI) are perhaps the most direct hedge against inflation. Commodities are also cheap by historical standards: they are the only major asset class to have declined in absolute terms over the past decade (the underperformance is significant and is largely due to falling energy prices). Since 2010, the S&P 500 has quadrupled, while the S&P GSCI index has fallen by nearly 40%.

Among stocks, focus on value and a low-volatility, short-term investment style. Growth and quality stocks also have a negative correlation with inflation.

Expectations of higher interest rates are boosting “value” stocks, which are cheap relative to current earnings and can therefore be considered short-term plays. Meanwhile, “growth” stocks—which are expensive relative to current earnings and are therefore long-term plays—are struggling in relative terms. In this environment, the financial sector can provide a hedge against a sharp rise in long-term rates, while commodities offer a hedge against higher inflation.