The high premium that stocks continue to offer relative to real interest rates continues to justify their overweight allocation relative to fixed income.

Last week, we argued that, by balancing the negative factors (tighter policies and high valuations) with the positive factors (low risk of recession), investors are advised to maintain a more or less neutral risk exposure.( https://www.fynsa.cl/newsletter/politica-monetaria-2/)

This week, we'll take a closer look at what this means in practice in terms of the potential of U.S. equities.

It is true that the market has so far taken the Fed’s “tougher stance” relatively well, on the understanding that the Fed will be able to achieve “a soft landing for the economy” and avoid a policy mistake that could lead to a recession.

We agree that, for now, the risks of a recession are limited and that the U.S. economy is in good shape to absorb a less accommodative monetary policy; therefore, the expected growth in corporate earnings—around +8% for S&P 500 companies—would not be “at risk.”

However, as inflation risks remain high—at least through the first half of 2022— the market has been leaning toward a more aggressive monetary normalization process than the one outlined by the Fed just a week ago; in other words, the guidance for the federal funds rate over the next two years (2.8%) could end up being brought forward almost entirely to this year.

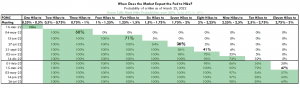

Evidence of this is that market expectations for further rate hikes at the May and June FOMC meetings have begun to factor in an increasing probability of a 50-basis-point hike per meeting (probabilities of +68% and +71%, respectively), reinforced by recent statements from Powell and other Fed members who have made it clear that price stability is the “priority” today. The attached table also shows that the probability of the rate ending this year at 2.8% has already reached 32%—a low but rising probability.

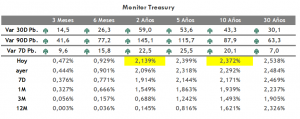

Of course, this is putting additional pressure on market rates, with the 2-year Treasury yielding over 2.1% and 10-year rates nearing 2.4%—levels we had actually expected for 2022, but which we now believe could be closer to 2.7%. This implies a further flattening of the yield curve and a potential inversion of the curve later this year.

With this in mind, we see very limited potential for earnings multiples to expand in the equity market, and the potential upside depends entirely on expected corporate earnings growth.

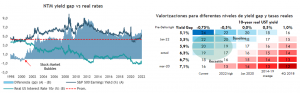

For now, the market is supported by real rates that remain highly accommodative (-70 basis points for 10-year bonds), levels we consider very low compared with other monetary normalization processes. While it is difficult to envision positive real rates, given the “greater tolerance” for inflation compared with past cycles, we do believe that real rates could very well move toward more neutral levels going forward.

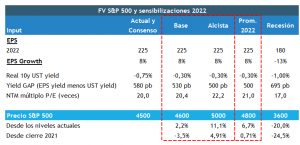

All in all, we are adjusting our projections for the S&P 500 to 4,600 points, consistent with an expected EPS of US$225 per share, a forward P/E multiple of around 20x, and real 10-year rates of -0.3%. This implies some compression of the equity risk premium (ERP) from the current 580 basis points to levels closer to 530 basis points, which are essentially the levels seen prior to the geopolitical crisis in Ukraine.

The high premium that stocks continue to offer relative to real interest rates continues to justify their overweight allocation relative to fixed income.

Since this is a recurring question, we are factoring in the possibility of a potential recession scenario, using the average decline in EPS during recessions (-13%) as a baseline; under this scenario, the S&P 500 would fall to around 3,600, matching the median decline during recessions (-24%).

If geopolitical and inflationary pressures ease later this year, our bullish scenario calls for levels closer to 5,000.

Humberto Mora

Strategy and Investments