So far this year, the MSCI EMU Index has posted a total return of 15% in U.S. dollars. The MSCI U.S. Index has managed only 12%. Going back to early November, when hopes for COVID-19 vaccines began to boost the markets, the return gap is even more pronounced. Eurozone equities have returned 44%, compared with 31% for U.S. equities. The eurozone has outperformed despite starting vaccinations later and having a slower start to its vaccination programs. As a result of these delays, European countries are only now beginning to ease restrictions on economic activity. This suggests that eurozone growth has room to surprise on the upside, and that eurozone stocks may still generate further gains.

As vaccination programs have accelerated and service industries have begun to reopen, opinion polls have rebounded. Data released this week showed that France’s business confidence index rose to its highest level in three years in May, with confidence in the service sector on the rise. Similarly, Germany’s IFO survey of business expectations posted its strongest reading since January 2011.

As a result, the European Commission’s recently updated forecast of 4.3% annual growth for the eurozone appears too conservative. A figure above 4.5% seems more likely, and possibly as high as 5%.

This suggests that there is still likely to be further upside for the cyclical stocks that have led the recent rally: the former “Covid losers,” including banks and traditional retailers.

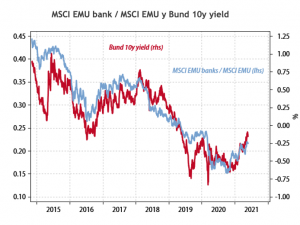

With a total return in dollars of 99% since late October 2020, eurozone banks have likely already seen the peak of their performance. However, there are good reasons to believe they may still offer some additional advantages.

Traditionally, the performance of eurozone bank stocks relative to the broader index has been highly correlated with the slope of the yield curve. With the European Central Bank’s pledge to keep official interest rates unchanged until inflation is “consistently” at target, the very short end of the curve will remain anchored in negative territory well into the medium term. As a result, the slope of the curve—and thus the relative performance of bank stocks—will be driven by movements in 10-year yields that carry upside risk.

Among the other “Covid losers” that are likely to continue outperforming are brick-and-mortar retailers. Hard hit in the early days of the pandemic, they have recently regained ground at the expense of online retailers. So far this year, stocks in the traditional retail sector have risen 15%, while stocks in the online retail sector have fallen 7% on average. This trend is likely to continue as European economies reopen.

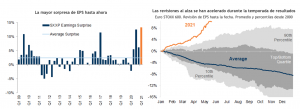

Finally, the visibility of corporate earnings has been improving significantly in Europe, with Q1 2021 results far exceeding estimates. (see charts)