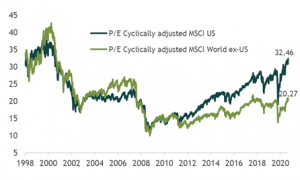

While valuations are historically high for U.S. stocks, especially for “growth stocks,” this is not usually true for stocks outside the U.S. The Shiller-type CAPE (cyclically adjusted P/E) for non-U.S. markets is as low today as it was 20 years ago.

Long-term returns on U.S. stocks are expected to fall to lower levels in the coming years as a result of a mean reversion and to reflect very low interest rates. But outside the U.S., this mean reversion has already occurred, as has the adjustment to very low risk-free rates. In fact, the mean reversion in Europe, Japan, and the UK would suggest higher equity returns over the next decade, in contrast to the lower returns implied by the overvaluation of U.S. stocks. Therefore, the rotation from U.S. to non-U.S. markets that began late last year is likely to gain momentum. The same should be true for the rotation from growth to value.

And in the case of emerging markets, despite their strong performance in recent months, they are still trading at a discount of more than 20% relative to the developed world.

It is interesting to look at the post-financial crisis period (through the end of 2010), marked by massive monetary stimulus, a weak dollar, and a commodities bull market, which can certainly be compared to the current period, during which emerging market stocks came to trade at levels once seen in developed markets.

MSCI US vs. MSCI World ex-US Cyclically Adjusted P/E (CAPE).

Relative Performance of the MSCI EM vs. the MSCI World