At the beginning of the year, we argued that the risk of market corrections had been increasing (https://www.fynsa.cl/newsletter/estrategia-internacional-2/), in light of higher interest rates resulting from the Federal Reserve’s monetary normalization process.

Fast forward to today, and the S&P 500 is down 6.0% for the year (having fallen nearly 10% as recently as a week ago), while the Nasdaq—given its greater sensitivity to interest rates—has seen losses double those of the S&P 500. And even though the overall outlook for corporate earnings remains solid, concerns persist about the Federal Reserve’s tightening and fears of stubborn inflation, which continues to feed back into highly strained supply chains, energy prices under pressure from geopolitical tensions (oil is already trading at US$90 per barrel), and wage pressures that were most evident in this week’s employment data.

To complicate matters, it is not just the Federal Reserve that has been stepping up its rhetoric regarding an earlier—and likely faster—withdrawal of stimulus measures; most major central banks (with the exception of China) are also accelerating the withdrawal of these measures.

First (among the major central banks) was the Bank of England, which surprised investors with a rate hike in mid-December (after promising it wouldn't do so), and then this week ended its quantitative easing (asset purchases) and raised rates again.

Also this week, European Central Bank (ECB) President Lagarde signaled an aggressive policy shift in light of heightened inflation risks, leading to expectations of a substantially earlier policy exit.

In fact, speculation about monetary policy normalization has even reached Japan, the most moderate of all developed economies.

In practice, in the case of the U.S., the market is already pricing in five rate hikes by the end of the year (and a 25% probability of a 50-basis-point hike in March); asset purchases are set to end in March, and an early start to QT (balance sheet reduction) is even being considered.

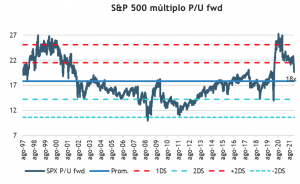

Against this backdrop, interest rate pressures remain high, weighing on market valuations. From a fundamental perspective, rising interest rates have accounted for the entire decline in the S&P 500. The real yield on the 10-year U.S. Treasury note rose by 60 basis points (from -1.1% to -0.5%) between the S&P 500’s all-time high on January 3 and the day after last week’s FOMC meeting. Over that same period, the S&P 500’s forward P/E ratio fell from 21.8x to 19.5x, mirroring the market’s decline.

Of course, a recurring question these days is whether the worst of this correction is already behind us or whether we could still face further losses before the markets stabilize. As a reference, all else being equal, the S&P 500 would fall by approximately an additional 10% to 4,000 if real Treasury yields rose from the current -0.6% to 0%, and by 15% to 3,800 if they rose another 50 basis points.

In this regard, an S&P 500 at 4,000 points would be consistent with a return to the mean in terms of valuation (around 18x) and would likely represent a great buying opportunity.

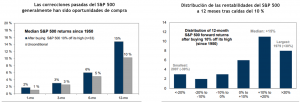

In a way, we’d “gotten a little used to” corrections that didn’t exceed 5% in 2021 and that the market quickly moved to buy into. In fact, we ourselves often promoted “buy the dip,” but clearly things have changed. But the question remains: Are corrections of 10% or more really that rare—without actually reaching a bear market (declines of more than 20%)? The evidence shows that they are not.

There have been 33 corrections in the S&P 500 of 10% or more since 1950. The median correction lasted approximately 5 months and involved a peak-to-trough decline of 18% (which in practice would be consistent with an S&P 500 level of around 4,000 points). An investor who buys the S&P 500 10% below its high—regardless of whether that was the low—would have earned an average return of 15% over the following 12 months (positive 76% of the time), and corrections rarely turn into bear markets unless the economy is heading toward a recession (which is not our base case).

Source: Goldman Sachs

Our recommendation has been to take a very conservative approach to duration in light of the risks posed by rising interest rates. However, just as we talk about “reversion to the mean” in terms of valuations in the equity market, a similar approach can be applied in the fixed-income market.

Corporate spreads for the U.S. investment-grade (IG) category have risen by about 25 basis points, a relatively limited and orderly move. This makes sense: the economy is performing well, and corporate balance sheets are robust. But with increasing interest rate pressures, we shouldn’t be surprised by further increases as spreads converge toward average levels of 130 basis points (a move very similar in practice to the tapering of 2013).

One positive development—which should be viewed as an opportunity—is that yields are starting to look more “attractive.” Today, the category offers a yield of 2.8% (which could approach 3%); that’s more than 100 basis points higher than just six months ago, and in a world with such low interest rates, investors will surely be vying for these opportunities.

Humberto Mora

Strategy and Investments