I’ve been wanting to start writing for our newsletter for months, but honestly, I never seem to have the time—day-to-day life just sweeps us up, and I keep putting it off. However, after reading last week’s news about “VAMOS POR EL 100%,” I thought it was important to comment on the different pension systems around the world as a way to contribute to the discussion.

You may not remember, but in March 2006, the Marcel Commission was formed, and as if that weren’t enough, the so-called Bravo Commission was established in 2015. This, along with other efforts, demonstrates the importance that the pension system has held for various governments in our country. Many hours of work have been devoted to this, incorporating citizen participation, regional dialogues, surveys, and extensive research.

But… what's the bottom line here?

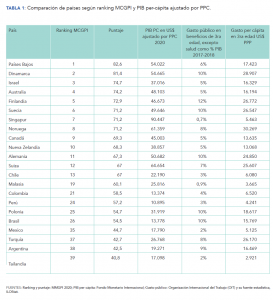

After researching pension systems around the world, I came to the conclusion that the work done so far is quite consistent with what has been observed in Australia, Norway, Switzerland, Canada, Israel, and the Netherlands.

The Marcel Commission noted that the Chilean system was unable to meet society’s demands, making reform necessary—though this did not mean dismantling the existing system. Global experience showed that the most successful reforms are based on an individually funded system, though it called for establishing a solidarity pillar, raising the replacement rate, increasing the retirement age, ensuring universality, intensifying competition, enhancing transparency, improving financial literacy, strengthening the voluntary pillar, implementing a basic solidarity pension (currently approximately $160,000 Basic Solidarity Pension (PBS) – SP. Superintendency of Pensions – Government of Chile (spensiones.cl)) and to establish criteria for the system’s long-term sustainability. Ten years later, all these concepts were adopted by the Bravo Commission, which also reached similar conclusions and put forward three proposals, ranging from maintaining the current system to returning to a pay-as-you-go system[1].

Currently the best pension system in the world (as ranked by the Mercer CFA Institute Global Pension Index) is that of the Netherlands. It features a universal basic pillar, which operates as a pay-as-you-go system, with employee contributions set at 18.25% (10% in Chile), plus a second occupational pillar, where companies, together with employees, contribute between 4% and 7% of salary to a private pension fund (which can be withdrawn under certain conditions) and an individual savings account. Through this system, they aim to achieve replacement rates of 70% of their final pre-retirement income, with a cap of 100%. Additionally, there is the Australian system (Age Pension Age Pension – Services Australia ), which features a solidarity pillar (funded through taxes and providing up to USD 1,162 per month), along with another pillar called Superannuation, which operates similarly to our system. However, there is one small difference: participants can choose from more than 85 different funds (for example, you can invest in an ESG fund). Finally, it also includes a voluntary pillar.

Given all this local and international (OECD) experience, I am concerned to see how some politicians have proposed withdrawing all funds, under the slogan “LET’S GO FOR 100%.” I believe it makes more sense to reach an agreement (common ground?) that reduces uncertainty in this area. This should be done not only for the sake of pensions—after more than 20 years of study and, let’s face it, waiting—but also because of the positive externalities it generates for the economy, where a deep financial system has enabled a large portion of the population to access affordable loans to buy their long-awaited home. As an example, I recall that 30 years ago, mortgage rates were quoted at UF +10% (1990), whereas today they can easily be found at UF +3%; I believe that, in terms of well-being, the benefits have been far greater. Furthermore, a deeper capital market opens up more financing opportunities, allowing all of us to aspire to become entrepreneurs.

[1] I disagree with this, although, as a result of the 2008 crisis, many Eastern European countries adopted this approach.

Francisco Muñoz

Partner – Sales Director at Fynsa