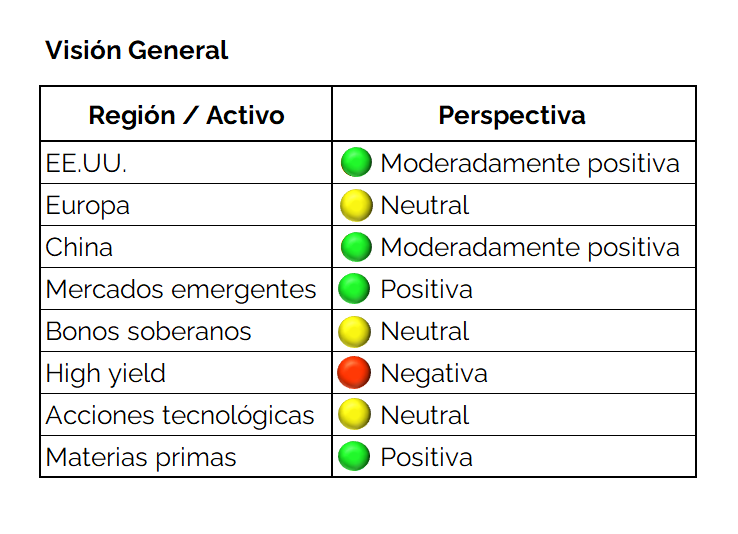

The general consensus is that the global economy, especially that of the US, is showing resilience despite the issue of tariffs, the presence of a labor slowdown, and some geopolitical tensions.

- Our base scenario is that there will be no recession in 2025–2026. In this regard, the superior performance of ex-US markets this year would extend into 2026, also leveraged by a weaker dollar and more attractive relative valuations.

- Growth is mainly sustained by:

- Massive investment in AI and data centers.

- Active fiscal policy.

- Consumption, mainly in high-end segments.

- China stabilizes and Europe continues to lag behind but with positive signs.

- In terms of sectors, we prefer Technology, Utilities, Banks, and Health Care.

- We also find commodities attractive for 2026. Supply constraints and higher demand support energy and metals.

AI: the dominant force of the cycle

Artificial intelligence is the most important structural driver for the economy and markets. U.S. growth is leveraged on AI.

- We are not in an AI bubble, although we are in a cycle of exuberance where technological leadership sustains high multiples.

- Capex in AI infrastructure will continue to accelerate until 2027, driving productivity but also labor disruption.

- Energy and regulatory policies will become increasingly relevant.

- The greatest structural risks are:

- Electric power.

- Infrastructure.

- Water for data centers.

- Financing.

- Circular Risk

Fixed Income: We prefer accrual over duration

- Given the fiscal tensions, we believe we should maintain an intermediate duration so as not to face volatility.

- Fed rate cuts will be slow and data-dependent.

- In our opinion, we believe that we should be invested in high-quality (investment grade) corporates and be cautious about large issuances in the technology sector.

- Back to Chilean bonds or Emerging Markets.

Equities: We remain positive

- Technology.

- Results revised upward.

- On weighing quality and balance sheet strength.

- Expand positions in Asia and emerging markets.

- Incorporate real assets and commodities.

- Integrate direct and indirect exposure to AI infrastructure, evaluate China

Inflation

Inflation is no longer as we know it; that is, it does not follow the same patterns, because:

- There is an energy shortage and supply constraints; we are in the midst of an energy transition, so we must ensure that we are prepared.

- The average rate increase today is 14%.

- Salaries.

- Massive investment in AI.

- Commodities: Copper | Lithium

For this reason, we believe that inflation may be more volatile.

The dollar | Fragmentation

The dollar is undergoing a significant transition, influenced by fiscal issues, rate cuts, and stronger growth outside the US. We believe it will continue to decline, but its hegemony is not at risk.

In the long term, the world is moving toward a multipolar monetary system:

- More use of other currencies, but none can compete as a reserve currency.

- This fragmentation process is driving the use of new regional or emerging currencies, and commodities (gold, oil, copper) may benefit from a slightly weaker USD.

- However, in technology, energy, finance, and capital:

- The US maintains its leadership.

- AI reinforces the dominance of the USD in the world.