If you are a regular reader of our newsletter, you may have noticed that our strategy notes have recently focused on international markets. This is no coincidence, as our goal has been to highlight the wide range of investment alternatives and opportunities, in addition to the advisory services we offer our clients in those markets.

That does not mean we have neglected our local investment opportunities, but we understand that, given the lack of visibility and the greater volatility of local assets, it is our responsibility to promote a more comprehensive, diversified, and globally focused approach to investment management.

That said, we believe this may be a good time to reassess opportunities in local markets

The first round of the presidential election brought a few “surprises.” The fact that Kast and Boric advanced to the runoff was the widely expected outcome of the first round and the result that virtually all polls had predicted. However, Kast’s lead of nearly 2% was less widely anticipated and is one of the reasons the market reacted positively to the results, as it gives him additional momentum heading into the runoff (a trend that will likely be confirmed in the first polls).

The biggest surprise in the presidential election was that Parisi came in third, defeating both Sichel and Provoste, the candidates from the traditional political coalitions. While it is difficult to place Parisi on the political spectrum, his voters will now play a key role in determining the winner in the runoff election.

In principle, Parisi’s main initiatives bear a closer resemblance to Kast’s than to Boric’s, including, for example, immigration issues; his proposal to achieve efficiencies in public spending in order to redirect resources toward pensions, health care, and education; his idea to lower the corporate tax rate and differentiate it based on company size; and the fact that, despite calling for greater regulation, he believes in a private pension system based on individually funded accounts. That said, “vote transfer” has never been linear in past elections, and consequently, it will be very important to monitor in the coming weeks where these voters are heading.

That said, from a broader perspective, we believe the main positive surprises came from the legislative elections, with the center-right gaining significant ground and securing 50% of the Senate. One of the main questions leading up to the elections was whether the center-right could retain one-third of the seats in both chambers. The May 2021 elections for mayors, governors, and constitutional assembly members had resulted in a sharp decline in representation for the governing coalition . This time, however, the outcome was the opposite, with the center-right gaining ground, securing 50% of the seats in the Senate and 44.5% of the seats in the lower house. In the latter case, this figure does not include the 3.9% obtained by the People’s Party.

Having a balanced Congress is very important, especially in this context, since any change to the rules governing the work of the constitutional convention requires a two-thirds majority in Congress (a constitutional amendment) to be approved. As a sign of this, greater representation of the center-right is also positive, as it will lead to a balance of power within Congress, with an eye toward the future government as well.

What’s next? A likely shift toward moderation in search of the middle ground. We believe the market will welcome this shift, as it could reduce uncertainty about the future. Signs of this have been evident throughout the week—for example, in the adjustments made to both candidates’ economic teams—though so far there have been no very specific proposals that would allow us to draw further conclusions.

Let's talk about strategy

How should the market react? Initially, the reaction was quite positive, although it has gradually faded as the days have passed—a trend also explained by a less favorable international environment. But beyond short-term volatility, we believe the market should interpret these results positively, and there is good reason to do so. The confirmation of a Kast-Boric runoff eliminates some of the tail risks embedded in the election (such as the absence of right-wing candidates in the runoff, for example), while the results of the parliamentary election—the biggest positive surprise—are positive not only as a political signal but also because they will likely moderate the actions of the other two forces that will coexist moving forward: the executive branch and the Constitutional Convention.

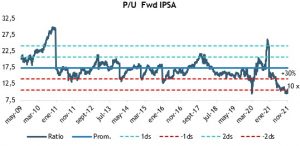

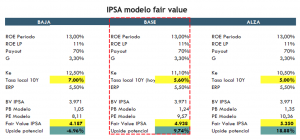

This new scenario should trigger a revaluation of Chilean stocks. It is important to understand that Chilean stocks carry a significant “institutional political risk premium” that currently has them trading at highly discounted valuations, with a 12-month forward P/E ratio of around 10x and a P/BV ratio of 1.2x. These figures compare with 10-year historical averages of 16.9x and 1.74x, respectively. While we do not believe the market will return to those multiple levels, a re-rating to the midpoint of the historical averages (-1ds) would imply a return of more than 30% based on both multiples.

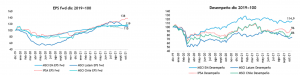

Otherwise, we have good corporate visibility (with reasonable uncertainties regarding 2022). The IPSA is on track to post earnings growth of more than 20% since the end of 2019 (vs. 15% for EM), while our profitability is 30% lower.

For now, we prefer to remain conservative regarding the target multiple, because we believe that, in the absence of “long-term visibility,” the market has focused on valuing “day-to-day” movements based on how interest rates change. In that sense, a sovereign yield at current levels (today at 5.6% for 10-year bonds) is already consistent with an IPSA index at levels closer to 5,000 points (which is, in practice, what the market had priced in before the recent corrections), whereas a rate around 5.0% (levels we consider closer to fair value) should be consistent with a nearly 20% rise in the IPSA, in our bullish scenario (considering current levels around 4,500 points).

Decline in investment

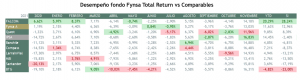

Today, at FYNSA, we have two investment funds that allow us to gain exposure to the scenario described above:

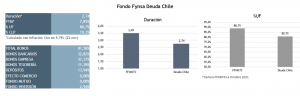

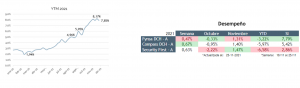

For local equities, the Fynsa Total Return Fund; and for local fixed income, the Fynsa Deuda Chile Fund.

While the market's ultimate direction will ultimately be determined by the outcome of the second round, the short-term market rally is likely to be driven by improved sentiment.

In the local fixed-income market, benchmark rates have room to adjust by at least an additional 50 basis points, particularly at the longer end of the curve, especially given the reversal of the fourth pension fund withdrawal measure. As a result, the performance of the local fixed-income market should continue the improvements already seen in previous weeks. In this regard, the Fynsa Chile Debt Fund currently offers an attractive risk-return profile.

Humberto Mora

Strategy and Investments