Investment Trends from Finanzas y Negocios on Vimeo.

Currently, the Private Debt market in the United States is undergoing strong changes with respect to what had occurred in previous years. The withdrawal of banks from this business, the increase in interest rates, and the mechanisms that exist to mitigate risks, are modifying the structure with which this type of loans are carried out, creating a highly attractive alternative for the entry of new players in this market.

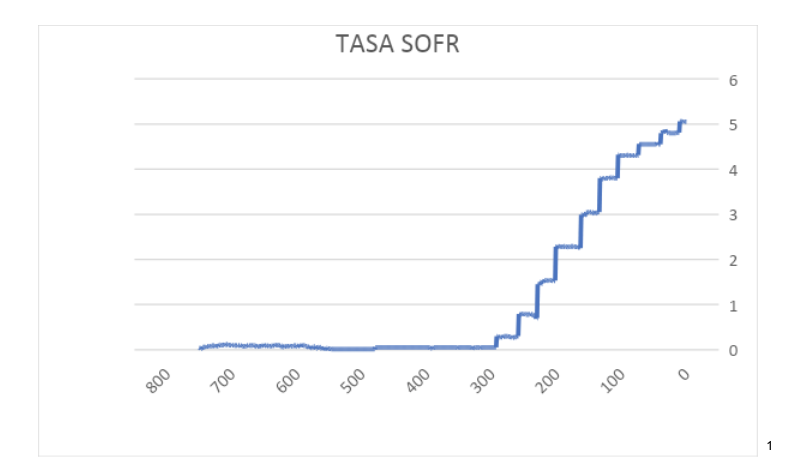

Due to rising inflation in the United States, the Federal Reserve was forced to raise interest rates starting in the first quarter of 2022. As a result, we have seen an increase in the rate of Secured Overnight Financing Rate (SOFR) from near zero, in January last year, to over 5% today, as shown in the chart below:

This increase in rates, at first sight, has two implications: The first is the growth of credit payment coupons, which means a higher return in absolute terms. But, as the theory goes, it also implies greater risk. In fact, taking into consideration the latest movements of the real estate market in the United States, especially in the case of commercial assets, it is observed that there is a higher vacancy rate and, in addition, lower lease prices than those observed in previous periods, so that the income for the borrowers of this type of loans has been strongly reduced. This, together with the increase in the cost of financing, results in a cash flow that is difficult to manage. This, together with the increase in the cost of financing, results in acash flow that is difficult to manage: there is a reduction in the "DSCR"(debt service coverage ratios), so that those who take these loans are obviously in a riskier situation than those who took them a few years ago, since they pay more and receive less.

But there is the other side of the coin: How can you take advantage of this situation?

To mitigate the aforementioned risk, the structure of these loans generally includes what has been called "Interest Rate Protection", a kind of insurance policy paid by the borrower at the initial moment of the loan. This has made it possible to capture the benefits derived from rising rates, while minimizing the logical risks involved.

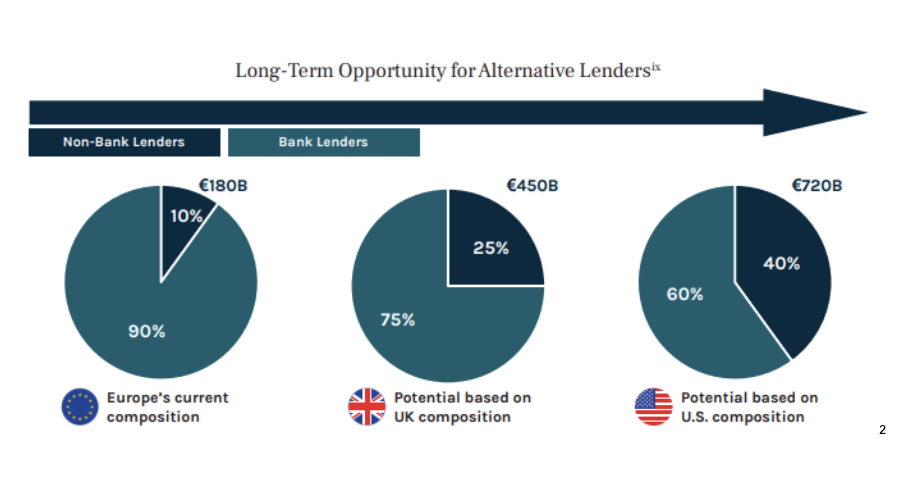

But that is not all, as it has been observed how banks are withdrawing from this type of business, leaving the way open for the entry of investment funds that act as the new lenders in this market, especially in the United States. In fact, as can be seen in the following graph, close to 40% of these operations are carried out by non-banks, marking a trend that is expected to continue to accentuate in the coming months.

On the other hand, this phenomenon helps these new players to be more selective when delivering such loans, having the possibility of opting only for businesses that are more attractive from the point of view of the debt-guarantee ratio. In this way, not only can the risk related to the interest rate be mitigated, but also the best alternative can be selected with respect to theLoan To Value and its respective underlying asset, in addition to the selection of the property managers themselves.

Thus, the Private Debt market in the United States is offering a new opportunity to be taken advantage of, with rates higher than those seen in recent periods and with mechanisms that help mitigate the logical risks of this equation. This, added to the greater selective capacity of lenders, generates a very attractive panorama, which is already attracting the attention of new funds and investors from all over the world.

Private Debt in the United States is offering a new opportunity to be taken advantage of, with rates higher than those seen in recent periods and with mechanisms that help mitigate the logical risks of this equation. This, added to the greater selective capacity of lenders, generates a very attractive panorama, which is already attracting the attention of new funds and investors from all over the world.

Martín León

Assistant Manager International Funds