Markets continue to trade volatility and lack a catalyst that could pull them out of their recent weakness, at least in the short term. On the one hand, there is pressure from geopolitical risks in Ukraine, which, of course, create uncertainty due to the disruptive effects that a military escalation would have (which is not our base case), and on the other hand, concerns persist regarding the U.S. Federal Reserve’s monetary normalization process, where the market (and we) have increasingly been leaning toward faster and more aggressive rate hikes given the heightened inflationary risks.

In a way, these two events feed into each other. Rising geopolitical tensions are making investors more cautious about the prospects of aggressive action by the Fed to tackle inflation. Immediately after last week’s very strong U.S. CPI report (+7.5% year-over-year), Fed fund futures were essentially fully pricing in a 50-bp move in March. But since the situation in Ukraine escalated last Friday, that expectation has retreated almost continuously, and futures now price in only a 38% probability of a 50-basis-point move next month. That said, if geopolitical risks subside, those probabilities will rise again, leaving the market essentially “stuck” in this position—a situation that will likely persist at least until mid-March, when the Fed will finally have to “clarify” its forward-looking outlook on rates and inflation.

But let’s get to the reason we’re here today… Last week, we argued that we believe we are at a turning point marked by some significant structural changes. The post-pandemic cycle is driving higher inflation and interest rates. (Embracing the New Reality: Strategies for a World with Positive Interest Rates).

And as we move forward at this turning point, the drivers of returns and market leadership are likely to be very different from those of the last cycle and should result in a different approach to investment strategy. Namely:

In particular, we believe the last two points are key in terms of positioning ourselves for the future.

Citi Research recently published an interesting study that examines these trends from the perspective of investment flows; its conclusions support our key convictions regarding asset allocation for 2022, namely: overweight in equities, underweight in fixed income, and overweight in commodities and non-U.S. markets.

Basically, the study concludes that there are three rotations currently underway

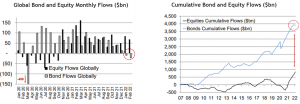

Rotation #1: Bonds to Stocks: Global bond funds are on track for two consecutive months of outflows (-US$32 trillion YTD), while stock funds have recorded inflows of US$153 trillion. These are significant shifts, but they remain small in historical context. Looking at cumulative flows since 2007, there is still a US$3 trillion gap between bonds and stocks. Perhaps a larger portion of that money could be reinvested in stocks should prices fall further. We are favoring a very conservative strategy in terms of duration and credit risk.

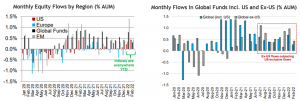

Rotation #2: From the U.S. to the rest of the world: Equity inflows have been strong across all geographies this year. However, investors are beginning to show a preference for cheaper markets outside the U.S. For example, flows into global funds excluding the U.S. have outpaced those into funds that include the U.S. for seven of the last eight months, as a percentage of AUM. For those looking to diversify outside the U.S., we are overweighting Emerging Markets, Europe (primarily the UK), and Japan.

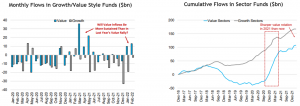

Rotation No. 3: Growth to Value: In line with this year’s price action, value funds have seen strong inflows relative to growth funds. However, this still seems modest compared to the value rotation in 1Q21. Looking at value-style funds, inflows peaked at around US$70 trillion last year, but have only reached US$20 trillion so far this year. Although the Q1 2021 rotation faded quickly, we suspect that its Q1 2022 counterpart could last longer. We are overweight the financial, energy, and commodities sectors overall.

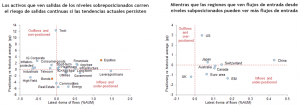

Finally, the positioning and fund flow landscape appears negative for inflation-protected bond funds, investment-grade corporate bonds, and certain equity sectors—particularly growth sectors (technology): these market segments are overpositioned (relative to historical levels) and are experiencing outflows. The outlook for fund flows may be more positive for European and emerging-market stocks, as well as energy stocks: these market segments are underweight (relative to historical levels) and are attracting inflows.

Humberto Mora

Strategy and Investments