We believe we are at a turning point marked by some significant structural changes.The post-pandemic cycle is driving higher inflation and interest rates.

As inflationary pressures become more evident—following this week’s U.S. inflation data, which showed a 12-month consumer price index of 7.5%—markets are beginning to lean toward faster and likely more aggressive monetary normalization. In practice, we’ve gone from pricing in five rate hikes by the Fed a week ago to seven hikes in 2022 (that is, a 25-basis-point hike at each meeting), with the likelihood of a 50-basis-point hike at the March meeting increasing.

Clearly, this has shifted the entire yield curve, with 10-year Treasuries trading above 2.0% and no foreseeable ceiling at this time (we believe a range of 2.3%–2.5% is reasonable).

As we move forward at this turning point, market drivers and leadership styles are likely to change. The drivers of returns and market leadership are expected to be very different from those of the last cycle and should result in a different approach to investment strategy.

The Shift in Interest Rates

Inflation expectations have risen rapidly. In the aftermath of the financial crisis, there was a sharp decline in aggregate demand and inflation. Inflation expectations fell, and the implied probability of high inflation—above 3%—plummeted, while the probability of inflation falling below 1% (the light blue line) increased . This trend has now reversed.

As a result, the shift in interest rate expectations has been exceptional. As recently as June of last year, the market did not expect any interest rate hikes in the U.S. in 2022, and as we mentioned earlier, it is now pricing in seven hikes by the Fed. Similarly, the dramatic shift in the forward guidance of other central banks has been exceptional. The UK’s rate hike to 0.5% was achieved in consecutive meetings for the first time since 2004 and represented the largest shift in the average of votes from one meeting to the next since 1997. In Europe—the epicenter of deflationary fears a few years ago—the market is pricing in a zero deposit rate for the first time since 2014.

The shift in inflation, coupled with more aggressive central banks, has led to a sharp decline in the proportion of bonds with negative yields worldwide—from about 25% to 5%—and the value of those bonds has fallen from a peak of US$18 trillion three years ago to about US$5 trillion today.

The Impact of Higher Interest Rates on Equities

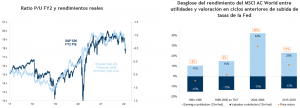

The first is that rising interest rates have pushed valuations lower.

This is not unusual. In recent cycles, while interest rates have generally risen (the extent of which depended largely on the strength of the economy), stock ratings have consistently declined , and ultimately, positive performance has been driven by corporate earnings.

The second impact is that correlations and risk premiums have begun to shift:

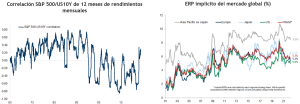

The correlation between stock and bond prices has been negative for most of this century.As bond yields fell to unusually low levels, further declines in yields (or rises in bond prices) were often accompanied by weaker stock performance. This made sense in a world dominated by recession and deflationary risks. Rising inflation, which has pushed bond yields higher in recent weeks, has weighed on stocks, resulting in a positive correlation.

The shift from deflation to inflation as the primary risk is significant. During the post-financial crisis era, the collapse of inflation expectations and the presence of central bank asset-purchase programs reduced term premiums in bond markets and, at the same time, raised risk premiums on stocks (which have more to lose from recession and deflation). The end of QE (asset purchases) and the shift toward QT (asset sales), along with higher inflation, should shift the balance in the opposite direction, reducing the ERP—a trend we’ve seen over the past year and one that likely has further to go.

Value Rotation

In the last cycle, investors were drawn to growth stocks. As aggregate demand collapsed, inflation expectations fell, and so did nominal GDP along with assumptions about long-term earnings growth. Growth became scarce and more valuable. Interest rates, which were falling steadily, increased the relative value of assets with longer durations.

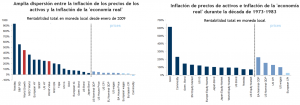

In the decade following the financial crisis, asset markets were re-priced by declines in the risk-free rate. The following charts show different measures of “inflation” around the world driven by the quantitative easing (QE) programs of 2009–2020. In the first chart, real-world inflation (the light blue bars on the right) was very low: consumer prices, wages, etc., barely moved, and commodity prices fell; interest rates plummeted, and central banks printed money. Meanwhile, inflation in financial assets (on the left in dark blue) was very high, and real returns were extremely strong.The best performers were the assets with the longest durations: the Nasdaq, the S&P 500, and growth stocks in general.

If we compare this to the inflationary decade of 1973–1983, we find a very different pattern. Most assets failed to generate a real return, as returns fell below the consumer price index. The best performers were “real” assets and commodities. The worst performers were the longer-duration stocks: the S&P and Nasdaq. While inflation on the scale of the 1970s is unlikely, it may well serve as a guide and makes the current market shift toward value investing seem rational.

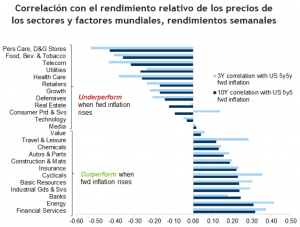

The shift toward value stocks in recent months reflects the turning point in inflation. As the following chart shows, the correlation between the sector’s relative performance and inflation expectations reveals a similar pattern. All sectors that consistently underperformed in the post-financial crisis cycle (which was dominated by deflationary fears) are those that are positively correlated with inflation expectations: energy, banks, and resources.

Recommendation

Our view, for several months now, has been that we believe we are entering a “more inflationary” cycle, in contrast to the past decade, which was essentially deflationary. Therefore, we are prioritizing value investments with short durations (and thus less sensitive to interest rate hikes) and positioning ourselves for a steeper yield curve (financial sector, energy). We are seeking greater diversification outside the U.S. in developed markets where valuations are more attractive (Europe and Japan), as well as in emerging markets that could begin to perform better in 2022 as China eases its monetary policy.

For fixed income, maintain a very conservative strategy in terms of duration.

Humberto Mora

Strategy and Investments