We remain constructive on risk assets based on the solid fundamentals underpinning the market: strong global growth, reopening and recovery following the pandemic, robust fiscal and monetary policy stimulus, and a solid consumer outlook that is expected to unleash pent-up demand. Recent market volatility has been largely driven by a market rotation away from high-momentum and expensive growth stocks, coupled with a adjustment in interest rates and inflation expectations, which should subside going forward.

- Although economic growth has exceeded estimates, it remains uneven across regions. So far, the United States and China have led the recovery, but this momentum has only recently begun to spread to Europe, and it will take even longer for it to reach emerging markets more broadly.

- In the specific case of the United States, both Treasury Secretary Janet Yellen and Federal Reserve Chair Jerome Powell want to keep the pedal to the metal to achieve maximum, inclusive, and broad-based employment. In this regard, it is essential to maintain support through asset purchases and low interest rates (accommodative financial conditions).

- The recent debate has centered on the risk of inflation. Rising commodity prices, supply chain issues (such as those involving semiconductors), declining global trade, and trade rigidities resulting from COVID-19 restrictions (in addition to a base effect) are cited as reasons for the rise in inflation, many of which are “transitory” in nature.

- In this regard, while the Fed is expected to consider beginning to scale back its quantitative easing (QE) in the coming months as the economic recovery takes hold, this process will be very gradual, and even after that, it could be many more months before interest rates rise. An early withdrawal of stimulus measures would be entirely counterproductive at this time, both for employment goals and for the higher inflation that the Fed has been promoting.

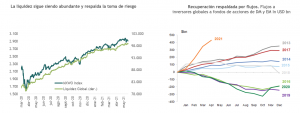

- The risks to the recovery include another resurgence of the virus, which is unlikely given the progress of the vaccination campaign. A credit crisis in a highly leveraged world also appears to be a potential problem, but one that is difficult to imagine given the economy’s liquidity. That liquidity is bolstered by a $4 trillion increase in the money supply.

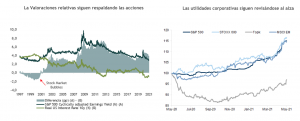

- Although the stock market is at record highs, the rally has extended beyond just a few tech stocks—in other words, market breadth has improved.

Is the market overvalued? Yes, but not as much as in other, more speculative cycles, and stocks still offer a high yield relative to benchmark rates. Furthermore, visibility into corporate earnings has improved significantly, with a global earnings recovery (MSCI World) approaching 40%.