Following China’s record year-over-year GDP growth in the first quarter (driven by the base effect and a massive credit boost), second-quarter GDP was expected to slow sharply (especially given the crackdown on investment and real estate deleveraging and the collapse of the credit boost).

Fears intensified after the People's Bank of China surprised markets last week by cutting the reserve requirement ratio (RRR)—the amount of cash banks are required to hold as reserves—a move aimed at boosting bank lending. The move has been interpreted as a further sign that China's post-pandemic economic recovery could be weaker than expected.

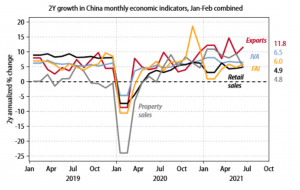

That said, fears of a sharp slowdown appear to be overblown so far: the official data for June remained strong (2-year smoothed data), with robust credit growth, continued strong trade, and sequential improvements in industrial activity and retail sales.

Looking ahead, certain risks remain, primarily on the investment side, linked to a slowdown in credit growth in recent months, a cooling housing market, the impact of decarbonization, and cost pressures on downstream sectors amid rising producer prices. Beyond that, as the bias of macroeconomic policy shifts from the restrictive stance in the first half of the year to a neutral stance going forward, credit momentum is expected to stabilize in Q3 and increase modestly in Q4. Along with consumption and services, as well as the ongoing favorable conditions for global demand, we expect economic activity to recover by the end of this year.

The economic cycle remained virtually unchanged in the second quarter