Recent price movements in sovereign debt markets are confusing on several levels. Yield curves around the world have flattened significantly.

Some possible explanations for the recent price movements are:

1) Concerns about the Delta variant are weighing on the outlook, particularly for regions with low vaccination rates.

2) the growing risks posed by a more aggressive Fed,

3) fading fiscal optimism, particularly in the United States, and

4) fears of a potential slowdown in China driven by policymakers adopting a more accommodative stance.

None of these are particularly satisfactory explanations, in our opinion, as we have noted in previous newsletters.

First, while the Delta variant has led to a rise in new cases in many regions, hospitalizations and deaths remain low in areas with high vaccination rates. As a result, we believe the economic impact on the U.S., Europe (and China) will be limited, although some parts of the world could see a greater impact on growth.

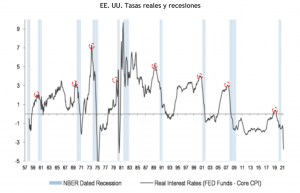

Second, while, in principle, an aggressive Fed should flatten the yield curve, the speed and the low levels at which the curve is flattening suggest that markets are placing significant weight on scenarios in which the economy cannot handle even a modest degree of policy tightening.

Furthermore, we believe that monetary policy will remain accommodative, with real interest rates remaining exceptionally accommodative, as will financial conditions.

Third, while there have been delays due to additional fiscal expenditures, the impact of the expected infrastructure initiatives is not that significant in the context of the measures that have already been approved.

Fourth, while a slowdown in global growth could certainly push U.S. yields lower, we have noted that fears of a deeper slowdown, particularly in China, appear to be exaggerated.

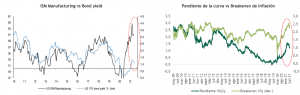

That said, the recent declines in long-term rates reflect the market’s perception of a slowdown in growth and a waning inflation threat—a view we do not share. We believe that long-term rates are at the bottom of this corrective process. We continue to target levels closer to 2% for the 10-year Treasury by the end of 2021, with a yield curve that will begin to steepen again. Consequently, we recommend a conservative strategy in terms of duration for international fixed income.