Just a few days after President Boric announced a new national lithium strategy, we at Fynsa organized a webinar to help our clients better understand the impact of this public policy on the development of the lithium industry in the country.

Of all the known aspects of this strategy, perhaps the most controversial one concerns the intention for the government to participate in the entire lithium production cycle, holding a majority stake in the event of a partnership with private entities.

The presidents of business associations have been highly critical of this announcement, primarily because of the leading role assigned to the government and the implicit lack of trust in private-sector management that this implies. And the criticism appears to be well-founded. A quick look at the performance of the public and private sectors within the mining industry itself is enough to understand the concern this announcement has generated. Codelco has serious operational flaws across all its divisions and project delays. Its production fell by 172,000 metric tons in 2022—the lowest level in 14 years—and its profits dropped by 63% compared to 2021. Our country’s leading state-owned enterprise faces serious competitiveness issues, a debt of US$18 billion, and a business model that, in the words of its current president, has run its course. In contrast, private mining companies (SQM and Abermale) contributed more than US$5,000 to the state in 2022 from lithium mining—double Codelco’s contribution to the Treasury and 39% of the revenue projected for the next twelve years.

And this is where the first question naturally arises: Why is it thought that the government can be a good manager in the lithium industry when it has not proven itself to be one in other industries? Today, five of the ten existing state-owned companies are losing money, two of which are potential lithium miners. Codelco earned US$4.4 billion less last year, while EFE, Metro, Enami, TVN, and Correos accumulated losses of US$376 million during the same period.

Given these figures, it is incomprehensible that a national strategy for lithium mining would not promote a virtuous partnership between the government and the private sector. In the proposed model, with the government as the majority partner, is there any possibility that a private company would invest US$700 million in the construction of a lithium plant when the company’s key decisions are made by the board of directors of a public enterprise whose membership is based more on political than technical criteria?

Chile has a unique opportunity to exploit this mineral that it must not let slip away. The growing interest in the lithium industry is driven by the projected growth rates in demand. While demand currently stands at approximately 700,000 metric tons, conservative estimates suggest it will rise to 1.6 million metric tons by 2025 and to 3 million metric tons by 2030. Among other factors, this demand is driven by the penetration of electric vehicles, which currently stands at an average of 12% and is projected to reach 45% by 2030. The largest markets for lithium will be in Europe and Asia, followed by the United States.

It is worth noting that these projections include new, growing market segments, such as energy storage. Demand in this sector could also drive an increase in lithium production and consumption, underscoring the importance of developing a robust policy for the industry.

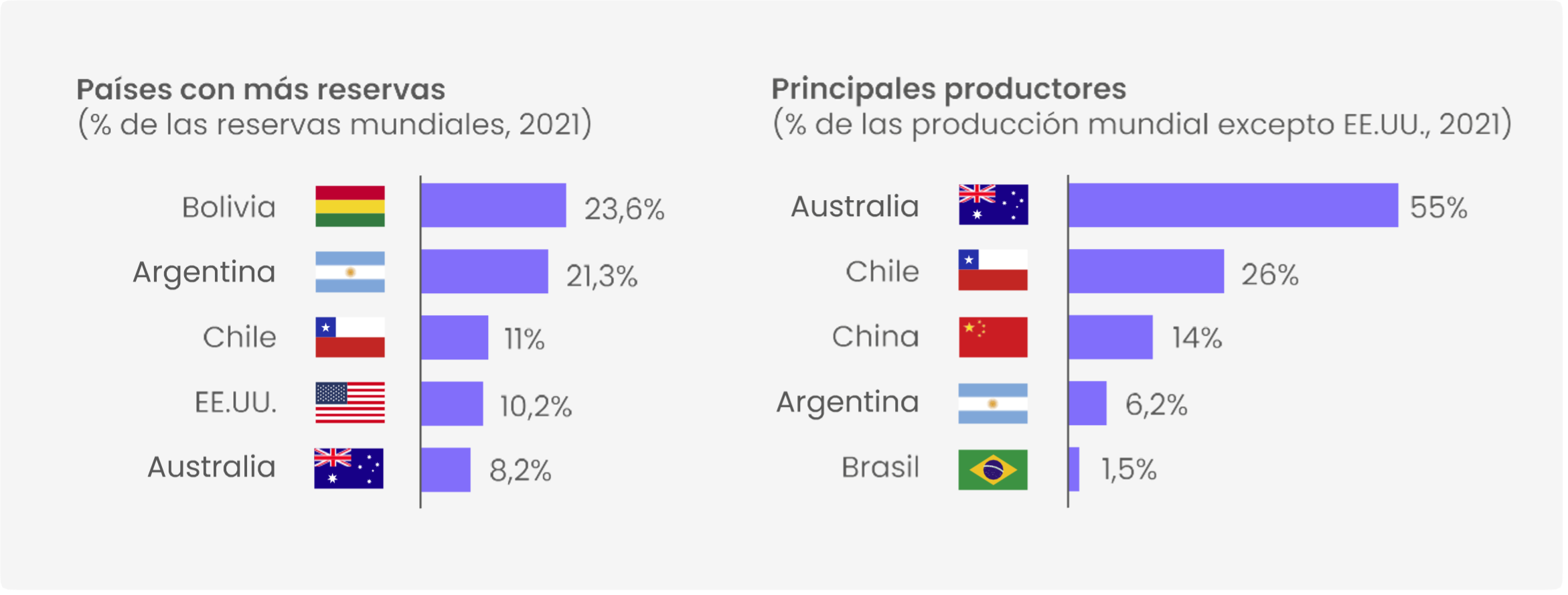

In terms of lithium reserves, Bolivia leads the way, followed by Argentina, which currently has more than 30 projects (it is important to note that some companies have been operating for more than 20 years). Chile, the United States, and Australia also have significant lithium reserves. However, although Australia does not have the largest reserves, it stands out as the world’s largest producer of lithium. This contrast highlights the importance of efficiency in lithium mining and production, regardless of the size of a country’s reserves.

Given this reality, it is urgent to accelerate the development of this industry in order to meet immediate demand. The time and cost involved in carrying out a mining project of this magnitude require swift action, and all signs indicate that we are falling behind.

Although there is still a long way to go and many challenges to face, we must closely monitor developments in the lithium market and the opportunities that arise. Collaboration between the public and private sectors will be crucial to the success and sustainable growth of the lithium industry.