Since our last update on local assets things have continued to develop favorably, with the IPSA returning 15% so far this year.

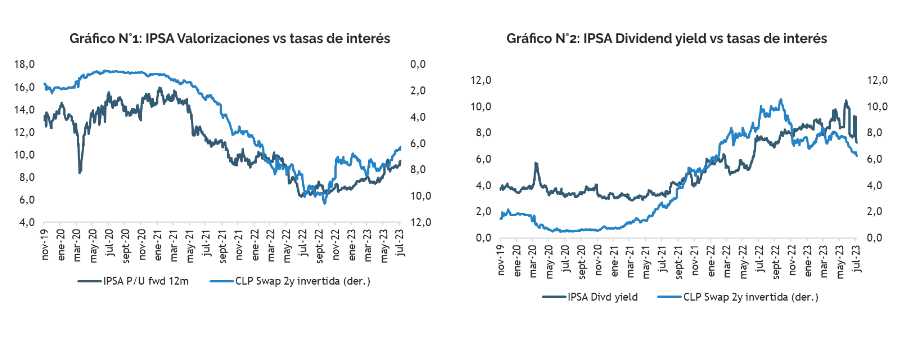

In addition to the reduction in political and institutional risks and highly discounted valuations, we can now add the expectation of aggressive monetary easing going forward.

The latest economic data, with downward surprises in both economic activity and, above all, inflation, clear the way for the Central Bank to implement its first rate cut of 75 basis points at the end of this month and end the year with a TPM of 8% (-300 bp), an adjustment process that would continue into 2024, bringing the rate to the 4.25%–4.5% range.

These lower interest rate forecasts not only mean greater potential for earnings multiples to expand, but also less pressure on the access and cost of financing front, in addition to making the attractive dividend yield on local stocks (around 8%) more “competitive.”

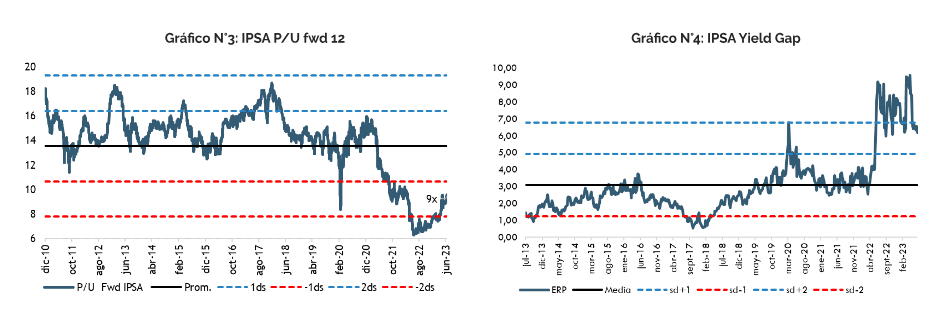

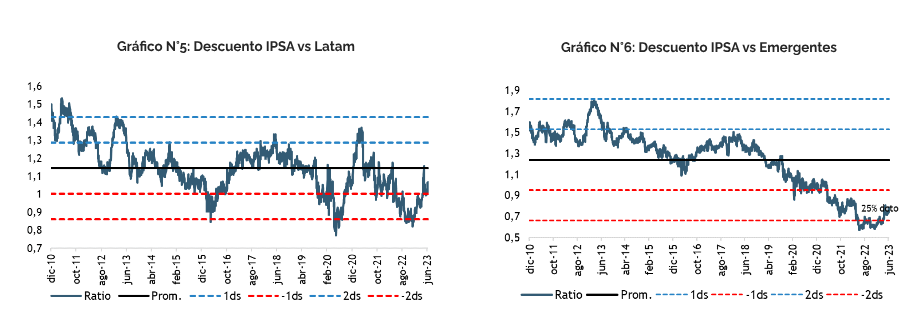

With regard to valuations, although they have been adjusting, they remain significantly undervalued by historical standards by any metric, both in absolute terms and relative to international comparables.

The IPSA is trading at 9x forward 12-month P/E, still significantly discounted relative to its long-term averages. Within the region, Chile is trading at a 6% discount to its averages and a 25% discount relative to emerging markets in general.

Similarly, interest-rate-adjusted returns are the most attractive in the region, with equities offering a premium of 600 basis points.

Looking ahead, we see room for further appreciation in local stocks. Investment flows from institutional, foreign, and retail investors have been increasing; positions remain light; and both the macroeconomic environment and corporate earnings are expected to improve heading into 2024.

For now, we are maintaining a 2023 price target of 6,500 for the IPSA (+8% from current levels), which implies a still conservative valuation of around 10x forward P/E. In our bullish scenario, which assumes a more favorable external environment (primarily driven by higher copper prices) and faster-than-expected monetary easing, we believe the IPSA could approach the 6,800–7,000-point range.

Finally, regarding our top picks, it is important to highlight the broadening of the local market, with more sectors participating in the recovery. Thus, we continue to overweight the commodities sector (SQM-B), but we also see opportunities in sectors more closely tied to the domestic cycle and more sensitive to interest rates, such as retail (CENSOSUD), real estate (MALL PLAZA), and utilities (ENEL CHILE), as well as consumer staples (ANDINA-B) and banks (CHILE).