- Amid a challenging start to the year for risky assets, the IPSA has managed to outperform global markets affected by expectations of rate hikes by the Fed and the recent global geopolitical conflict. The IPSA’s outperformance is mainly due to the strength of commodities and its “more value-oriented” composition (see attached table)—a characteristic shared by the region’s other stock markets—which, combined with attractive interest rate differentials, has attracted greater investment flows to the region.

Growth: Consumer Discretionary, Information Technology, Communication Services, Health Care (which have longer durations and are therefore more sensitive to higher interest rates)

* Value: Energy , Materials, Financials, Industrials (more closely tied to the “real economy,” sensitive to higher inflation, “short on duration,” and therefore less sensitive to higher interest rates)

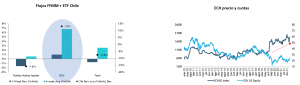

- In fact, foreign investors have been the biggest buyers of local stocks in recent months. New share subscriptions for the ECH (the ETF that tracks the MSCI Chile index) are at all-time highs.

- Thus, while global equities fell 5.2% in the first quarter, the IPSA posted a return of +24.5% in U.S. dollars, very close to the performance of the rest of the region.

- Sectors related to local economic activity and higher inflationary pressures stand out, such as banking (+24% year-to-date) and the commodities sector (+44% year-to-date), given the positive outlook for most local commodities (iron, lithium, and pulp). Together, these two sectors currently account for nearly 60% of the IPSA.

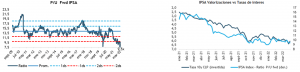

- Despite the IPSA’s strong performance so far in 2022—in contrast to global equities— we see room for further gains given that valuations remain attractive from a long-term perspective, both in absolute terms and relative to Latin American markets. While the domestic outlook will remain complex due to the political and institutional challenges we face in the coming months, the external environment offers some compensation, given the attractive prices of copper and commodities in general (iron ore, pulp, lithium).

- The geopolitical escalation has significantly increased the risk of further exacerbating the energy and commodities crisis that has unfolded over the past two years. Potential disruptions to trade in oil, gas, grains, and metals now pose a significant risk to investments and the real economy. Investors should, therefore, hedge against this risk by increasing their allocations to commodities, energy, and materials. These allocations would serve as a hedge against inflation and geopolitical risks.

- The “more moderate” tone set by the Central Bank regarding the future path of the policy rate has led to a sharp adjustment in market rates in recent days, which should ease pressure on already heavily discounted valuations and allow for some expansion of multiples in the short term.

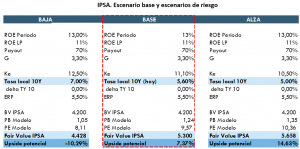

- All in all, under a still-conservative scenario, we are slightly raising our forecast for the IPSA to 5,300 points (+7.5%) and to +15% in our most optimistic scenario (5,650 points). This adjustment is justified by continued upward revisions to expected earnings for 2022 (+15% in March alone) and reduced interest rate pressures, following the more moderate stance on interest rates adopted this week by the Central Bank.

- We focus on selectively investing in stocks that we believe are undervalued (value), of high quality (solid financial position), and have growth potential. In terms of sectors, we are prioritizing commodities, banking, and consumer goods.

Decline in investment

Our Fynsa Total Return Fund provides exposure to local equities through an active, high-conviction strategy that maximizes alpha generation. For more details, click HERE

Humberto Mora | Assistant Investment Manager