The carry trade involves borrowing in a low interest rate currency to invest in assets denominated in a higher rate currency. Japan, with its historically low rates, has been a popular source for this strategy. However, recent changes in Japanese monetary policy have altered this dynamic, significantly affecting global financial markets. Investors convert yen into higher-yielding currencies, investing in assets such as the Mexican peso, U.S. Treasury bonds and technology stocks.

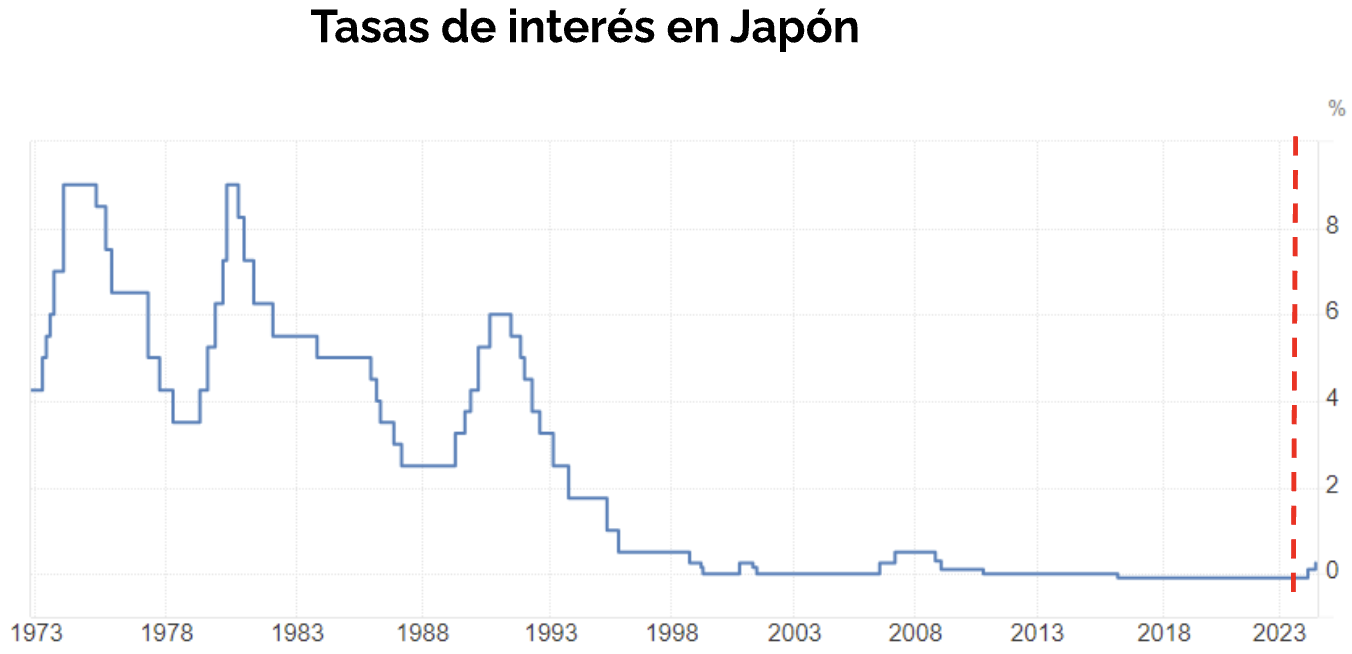

The change in Japan's monetary policy is notable, as the Bank of Japan (BoJ) raised interest rates for the first time in 17 years in March 2024, rising from -0.1% to a range of 0% to 0.1%. This increase reflects an effort to counter inflation and raise wages, after decades of negative interest rates and a yield curve control policy that kept long-term bond rates low. Subsequently, on July 31, the BoJ surprised the markets by raising its interest rate to 0.25%.

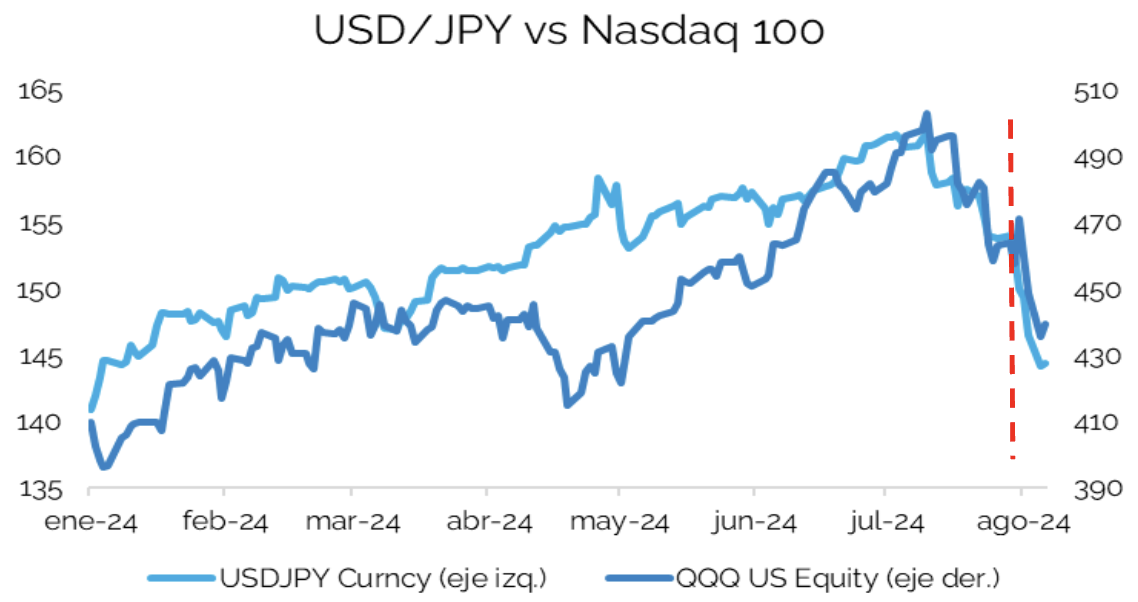

The sudden change in Japan's monetary policy, coupled with weak US labor market data, which has raised expectations of rate cuts by the FED (50bp in September), has forced investors to quickly liquidate their carry trade positions, generating a sell-off in several assets, has forced investors to quickly liquidate their carry trade positions, generating a wave of selling in several assets., This effect is amplified by leverage. The unwinding of the yen carry trade has impacted equity markets, as the yen has appreciated against other currencies and volatility has increased. Indeed, the VIX index reached levels not seen since the pandemic in March 2020.

The chart shows the relationship between the yen's appreciation and the Nasdaq 100's decline:

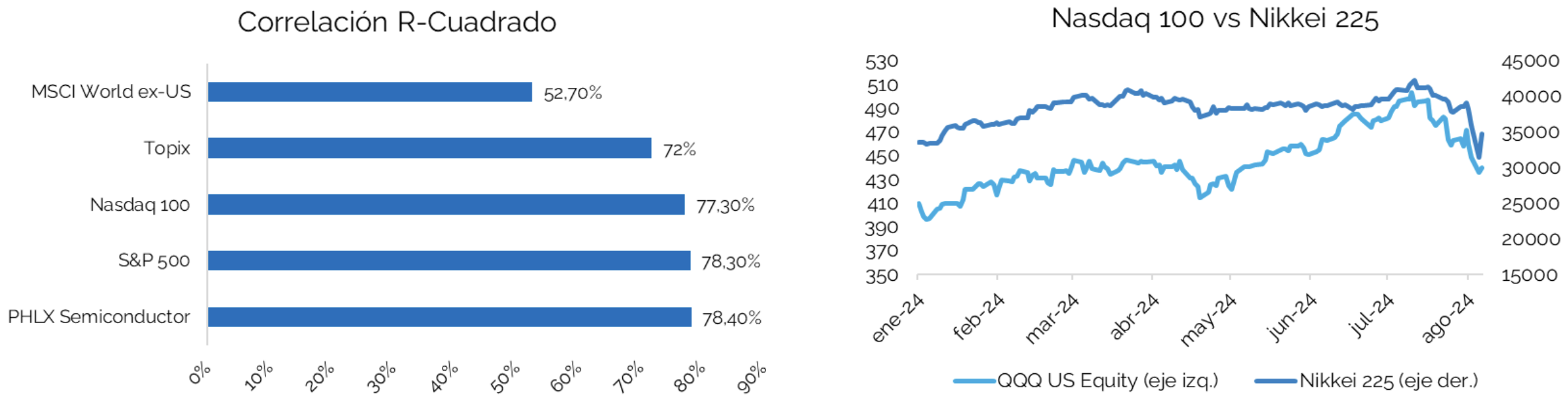

Against this backdrop, Japanese stocks suffered one of the biggest sell-offs in their history, falling by about 20% following the rate hike and accumulating a loss of 24% since their peak in July.. However, part of the fall has recently been reversed following verbal interventions by the BOJ, signaling that they will not raise interest rates again in unstable markets, limiting short-term risk. This impact was not limited to Japan, but affected global markets, showing a closer correlation with the S&P 500 and the technology sector than with the Topix itself, evidence that many carry trades have gone to finance part of the US market rally, as can be seen in the charts below.

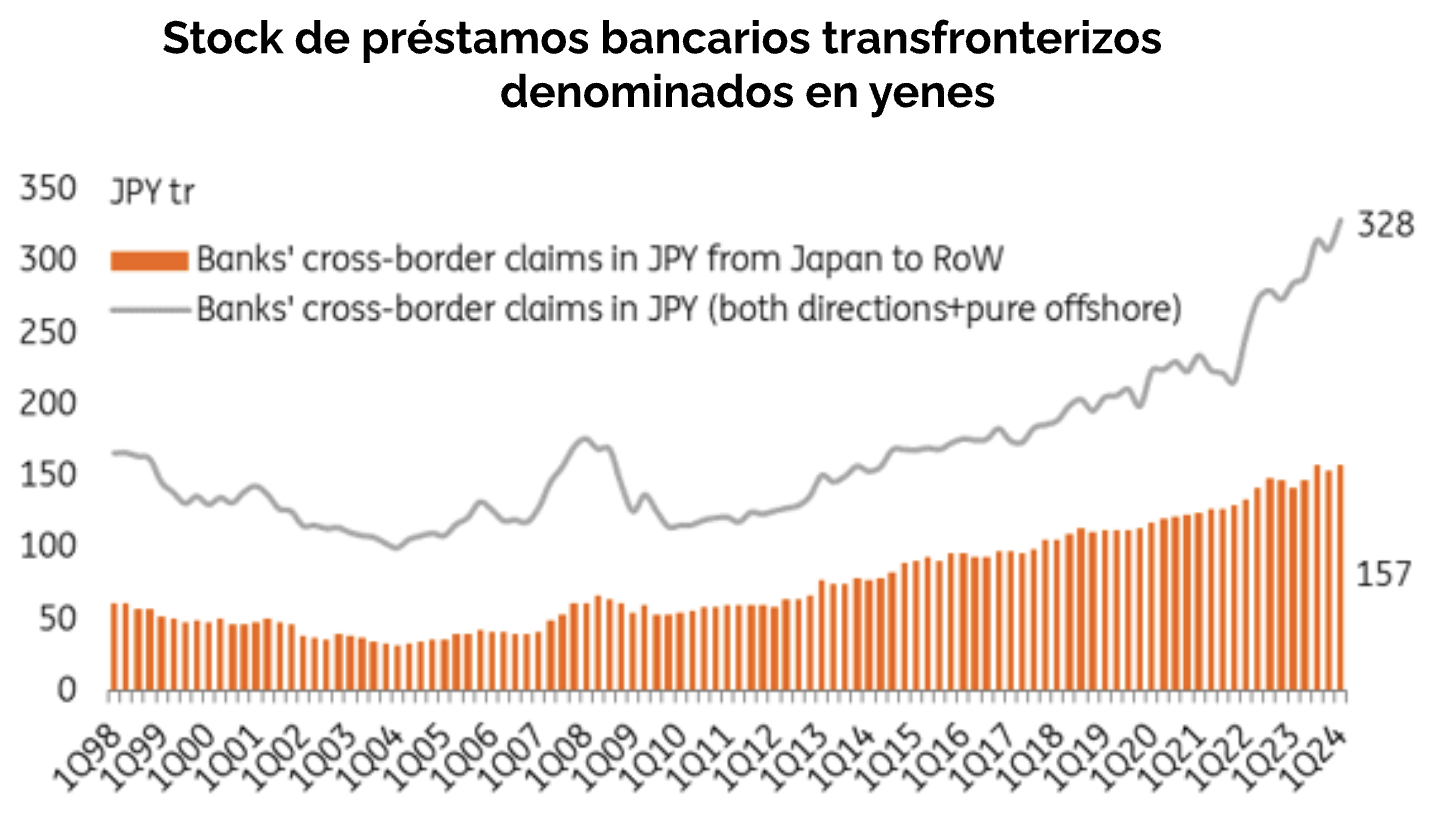

The next chart highlights the evolution of cross-border bank lending in yen.. Since 2010, international banks in Japan have increased these loans to JPY 157tr (US$1.0tr). The total includes loans from the Japanese country to the rest of the world (RoW), from RoW to Japan and loans offshore pure offshore loans at JPY 328tr (US$2.2tr). Data at the end of each period reflect an increasing trend, according to the Bank for International Settlements (BIS) and ING.

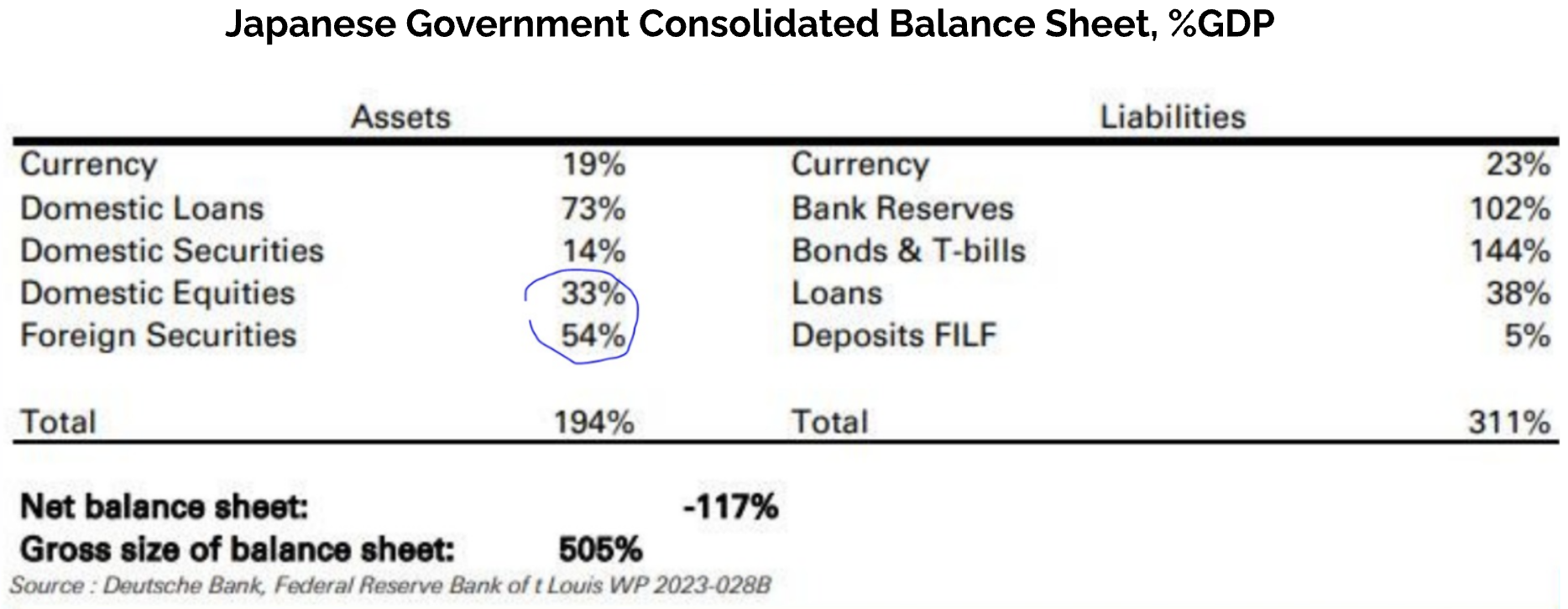

A report from Deutsche Bank suggests that the BOJ's huge balance sheet, which represents about 500% of the country's GDP, is essentially a giant carry trade. This implies that the BOJ is borrowing at low rates and investing in higher-yielding assets, possibly to support the economy or manage the value of the yen.

In conclusion, the dismantling of the yen carry trade, due to the BoJ's rate hike, has generated volatility in global financial markets. How much of the effects we have been seeing in the markets and potential impacts on financial stability may extend over time will certainly depend on the monetary policy decisions that may be taken not only by the BOJ, but also by the Federal Reserve itself.

That said, according to JP Morgan estimates, 75% of the global carry trade has already been eliminated and, for the time being, everything indicates that things are leaning towards the BOJ refraining from further rate hikes, all indications are that things are leaning towards the BOJ refraining from further rate hikes, as the FED will most likely start cutting rates as of September and this could put additional pressure on rate differentials with Japan.

Sources: Fynsa Estrategia, Bloomberg, BIS, CLSA.

Tomas Haase

Investment Analyst Fynsa