Current economic conditions have directly affected families' ability to purchase a home and realize their dream of homeownership, increasing the housing shortage, which, according to figures from MINVU, stands at 650,000 homes. This represents a 62% increase over the past 10 years, and over the next 4 years, the government plans to build 260,000 homes, making it the most stable housing program in Latin America.

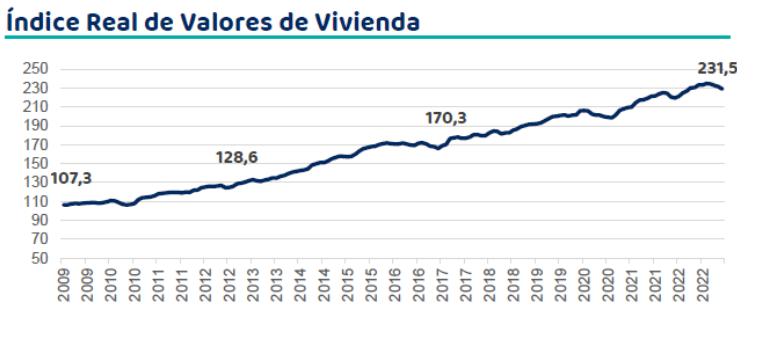

Added to this is the rise in housing costs in Chile, which grew by an average of 5.8% annually—adjusted for inflation—between 1990 and 2022, as well as the correlation with the increase in the savings required to purchase a home. The latter fell by 0.7% of GDP in 2022, reaching its lowest level in 20 years. As a result, 92% of people report not having the necessary down payment for a mortgage, according to the latest survey by Enlace Inmobiliario.

Access to Housing: Down Payment Loan

This is financing for people who do not yet have enough savings to take the first step and buy their own home today, at a time when banks require a minimum down payment of 20%. The loans are offered in fixed monthly installments with terms of up to 60 months and are intended almost exclusively for the purchase of a home. Furthermore, this initiative—in partnership with real estate companies—allows those companies to reduce their inventory of new homes, thereby boosting the real estate and construction industries nationwide and having a dual impact on the economy.

Benefits for the real estate market

Better sales results for both immediately available and future inventory, improving sales velocity and allowing real estate agencies to focus 100% on their business, allocate capital to their core business, avoid financial risk and collection costs, and recover funds in the event of default.

This type of financing also has a social component, since in some cases it is primarily aimed at the purchase of subsidized housing, with a focus on women and migrants, who face a greater gap in access to financing. This promotes sustained development, reducing inequality and fostering more sustainable communities in the long term.

Cristián Rodriguez P.

Private Debt Manager, Fynsa AGF