Growth and innovation in the private markets have driven the creation of new structures to meet different investor needs. While semi-liquid semi-liquid funds are valued for their ability to offer some liquidity with periodic subscriptions and redemptions, several papers have been showing that their benefits go beyond just liquidity.

Compared to traditional alternative funds that have capital calls in the first years of life, semi-liquid funds can offer immediate exposure to private markets, allowing them to remain invested for the term of the investor's choice, semi-liquid funds can offer immediate exposure to private markets, allowing them to remain invested for as long as the investor chooses, mitigate the J-curve and reduce the limited visibility we may have of the underlying assets in some strategies.

Here the first question investors ask themselves is, the more illiquid I should expect a higher return? The answer is yes. In closed-end funds we can expect higher returns that vary depending on the strategy, these tend to move on average in ranges of between 15-20%. On the other hand, the returns we can expect from semi-liquid funds range between 10-12%. However, this is where one of the advantages of semi-liquid products comes into play: the speed at which we put our capital to work compared to closed-end funds.

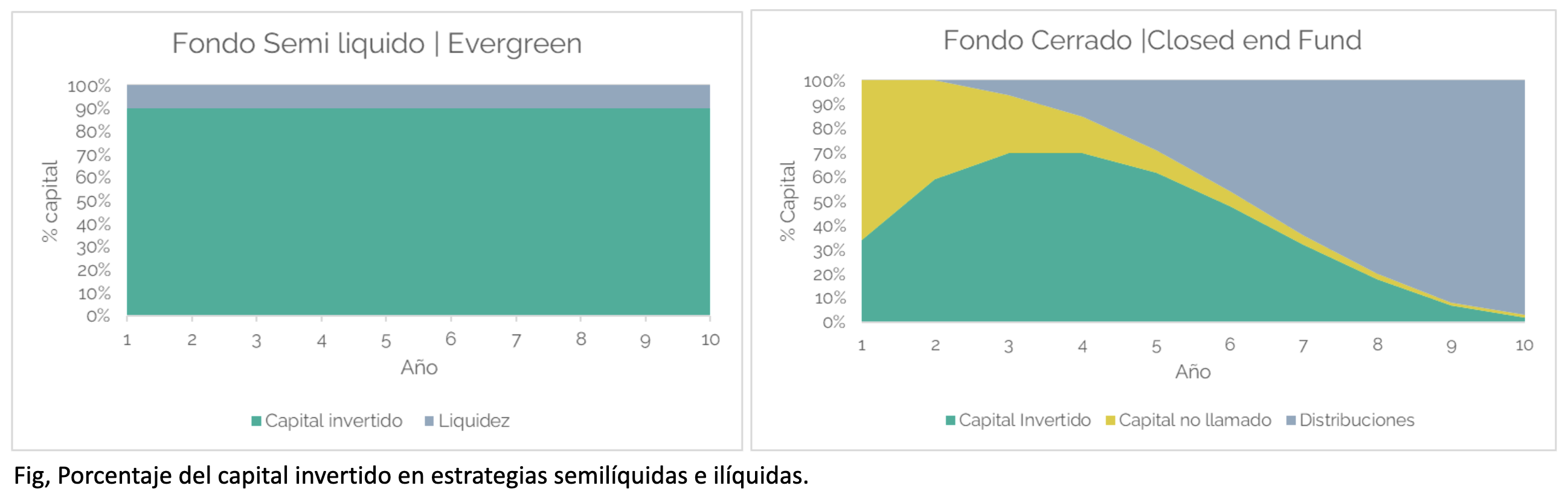

The latter, in the first years, call between 30-40% of the capital and this value increases to a peak close to 70%, where later distributions begin to be received, which lowers our exposure. In line with the above, UBS in 2023 gathered information from a large sample of funds and concluded that, on average, closed-end funds have 37% of their capital invested over an 11-year period. In contrast, semi-liquid funds will always be closer to 80-90% (Fig 1).

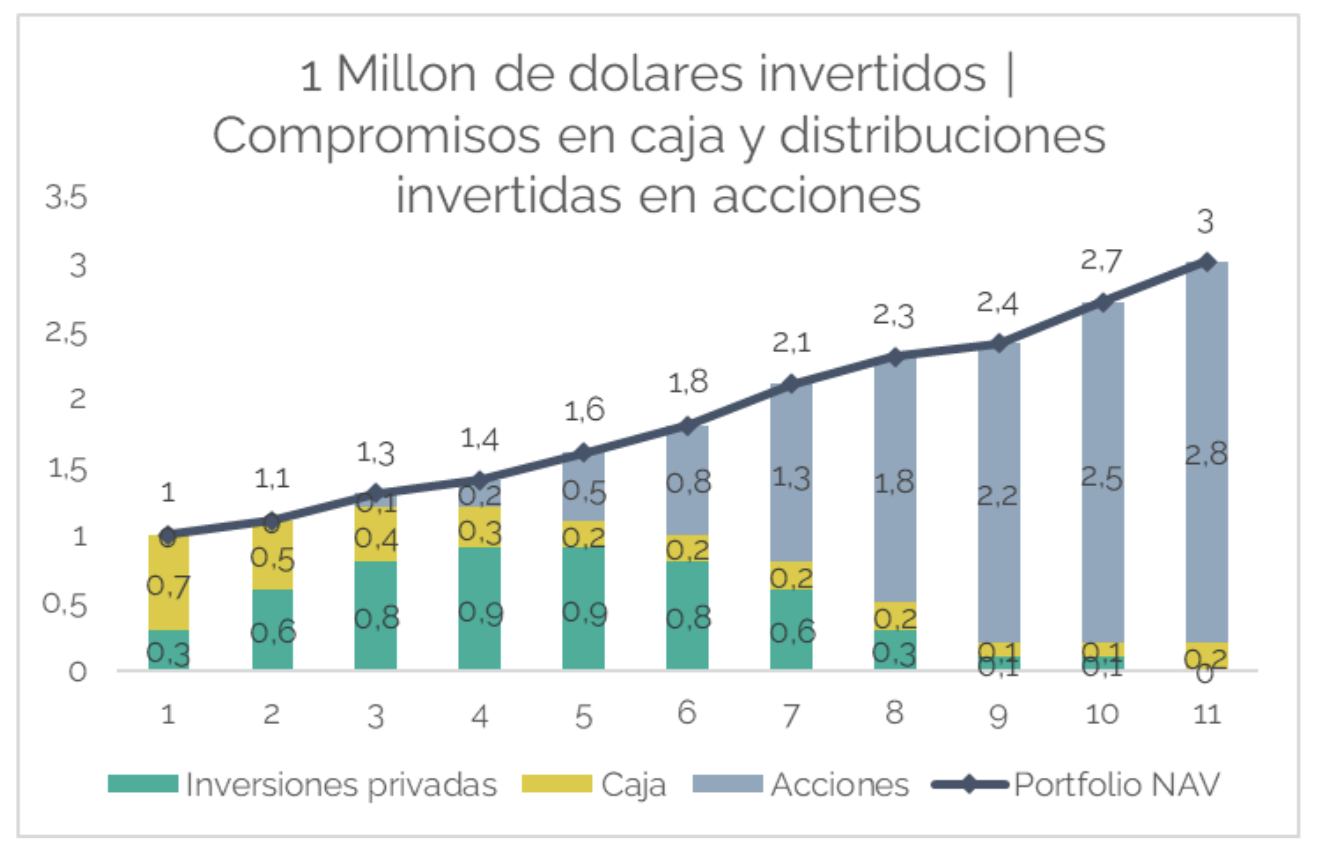

So, if I only have 37% of my capital invested, what do I do with the rest of the time? what do you do with the capital the rest of the time? This is the origin of a concept called Cash Dragwhich is nothing more than the dilution of returns due to the capital tied up waiting to be called in the next few years. Here, depending on the investor's profile, there are several ways to manage this cash. The further I move away from keeping this capital in cash, the more I risk not being able to meet capital calls in the event of a crisis where investments can easily fall by between 15-20%but, in turn, the expected returns are higher. The most commonly used strategies for cash management are:

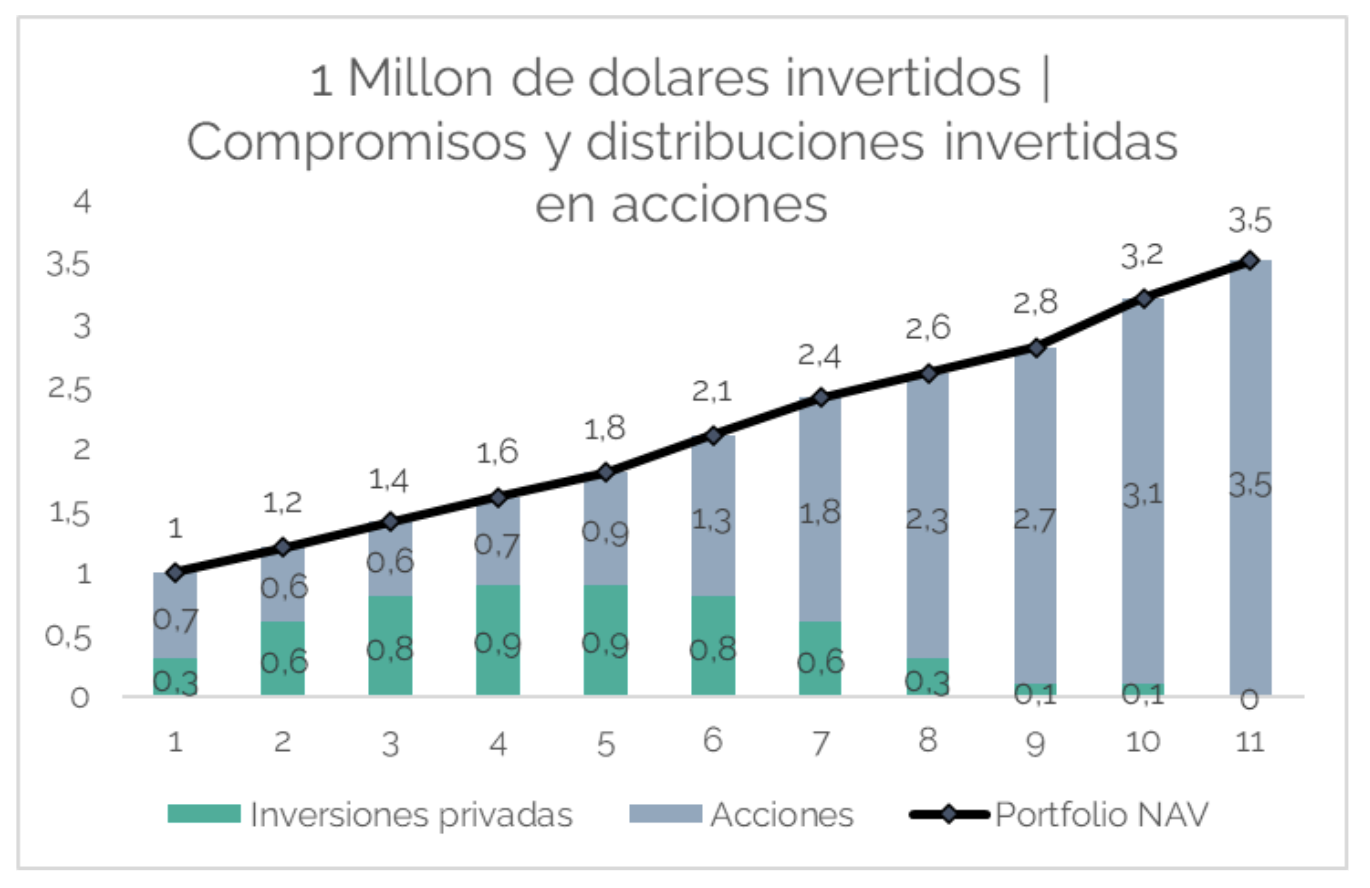

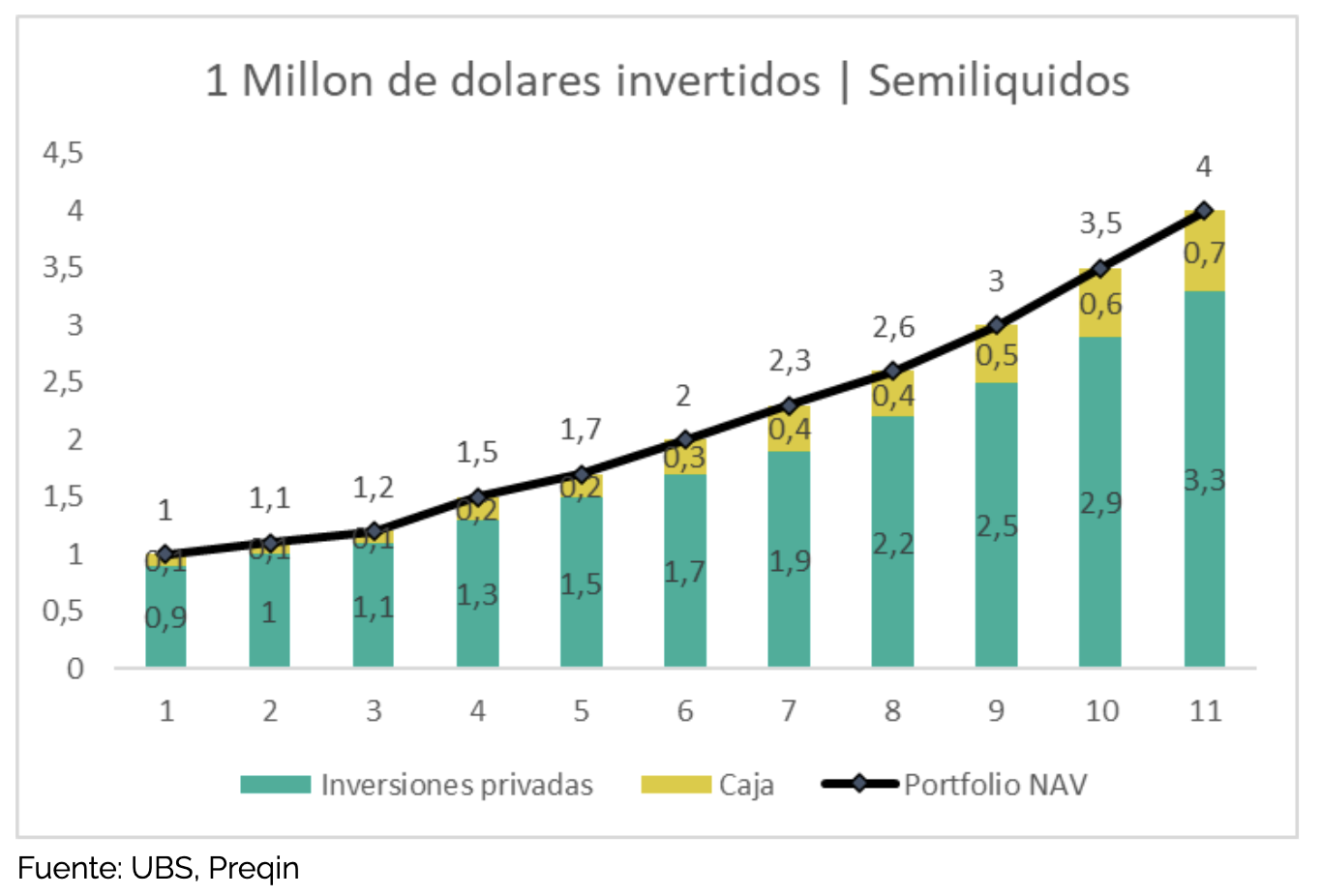

As we can see in the above exercise, $1M becomes $3M by using the strategy of keeping uncalled capital in cash, $3.5M by taking more risk and investing in the public market, while the semi-liquid strategy ends up at $4M as a result of having more of the capital invested for a longer period of time and reusing distributions.The semi-liquid strategy ends up at 4M as a result of having more of the capital invested for a longer period of time and reusing distributions.

Therefore, it is essential to have a good alternative program when choosing closed structures to mitigate this problem. Cash Drag as previously mentioned.

Family Office Team