We believe that these levels of divergence in the equity market are not sustainable and that a healthy correction should occur in the near future.

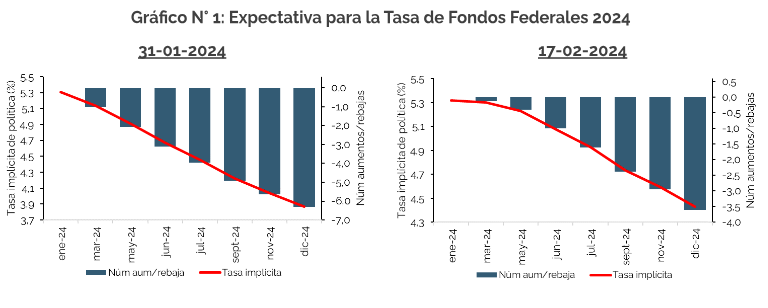

At the last Fed meeting, Powell reiterated the importance of strong data to support the 2% inflation target before considering interest rate cuts. At that time, the market initially anticipated 6-7 rate cuts, the market initially anticipated between 6 and 7 rate cuts, while the FED had previously mentioned that it would make 3 cuts over the course of the year (see Chart No. 1: 31.3%). (see Chart N°1: 12/31/2024).

Today, three weeks after the Fed's decision to keep rates in the 5.25% - 5.5% range, the market is now more aligned with the Fed's view (see Chart N°1: 17-02-2024), expecting between 3-4 cuts and shifting the first cut to June instead of March.

This revision by the market is due to a number of economic releases that were not in line with consensus expectations. For example, new jobless claims have been consistently lower than expected in recent weeks (218K vs 221K the first week after the Fed meeting; 212K vs 219K the second week; and now in the third, 201K vs 217K), while average hourly earnings in January rose 0.6%, beating the consensus of 0.3%. In addition, nonfarm payrolls for the same month surprised with an increase of 353K vs. the forecast of 187K. All of these data continue to evidence remarkable strength in the labor market, which is one of the leading indicators supporting the Federal Reserve's stance of not cutting interest rates until weaker data on this front is observed.

On the inflation side, the Consumer Price Index (CPI) also beat expectations by increasing by 0.3% (vs. 0.2% expected) in Jan, raising the year-on-year rate to 3.1%, above the consensus of 2.9%. The indicator most closely monitored by the Fed to assess inflationary trends is the SuperCore (the Core CPI Services Ex-Shelter Services Index), which jumped 0.7% m/m (the largest increase since September 2022), pushing the y/y change to +4.4%, the highest since May 2023.

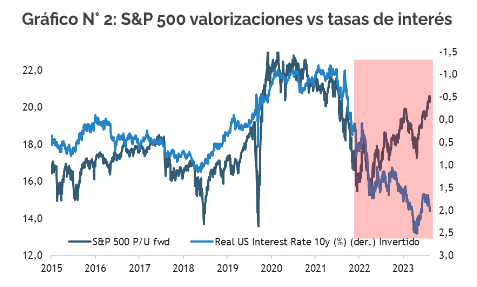

Finally, the Fed minutes released on Wednesday of this week revealed that most officials are still more concerned about the risk of cutting rates too soon than keeping them high for an extended period of time. officials are still more concerned about the risk of cutting rates too soon than keeping them high for an extended period. All of these strong economic data and events have influenced the market's perception of the Fed's monetary policy, which has been reflected in the fixed income market. The 10-year Treasury yield has risen from 3.9% to 4.3%, and real rates are again approaching 2.0% (see Graph No. 2).

However, we have not seen a correction in the equity market, even though technical indicators point to the market being overbought and reaching all-time highs. We know that the world of equities is not only subject to these data that we have exposed. It has maintained a great performance in recent times, mainly due to the strong earnings season of companies. However, how long will this dynamic be sustained in an economy that is likely to slow down in the coming quarters? We believe that these divergence levels are not sustainable and a healthy correction should occur in the near future (see Chart No. 3).

Felipe de Solminihac

Investment Strategist