There are several headwinds, including weaker global growth, concerns about inflation, rising input costs, tight profit margins, the Fed’s policy shift, and, most recently, concerns about China’s credit markets.

But let's take it one step at a time.

How concerned should investors be about the Evergrande issue?

To begin with, it's good to give a little background:

That said, while China could carefully manage any potential default or restructuring by Evergrande to protect the financial and real estate markets, it may need to do more. Economic data is already weak, and a clear message from the government is needed to shore up confidence and stem the domino effect. The absence of such action poses a significant downside risk to future growth.

In summary, we do not believe the sector faces systemic risks; overleveraged developers will gradually sell their assets with the support of the central and local governments when necessary.

In another significant development, the Fed strongly hinted that it will begin to taper its asset purchases after the next FOMC meeting in early November. This week’s post-meeting statement indicated that if economic progress “continues broadly as expected,” then a slowdown in the pace of purchases “could soon be warranted.”

The signal of a rate cut was eagerly anticipated, given the strong indications from previous statements. While there are certain conditions attached to the decision to gradually cut rates in November, Powell made it clear that it would take a major disappointment to derail them from their course.

But Powell went a step further, noting that “a gradual tapering process concluding in the middle of next year would likely be appropriate.” This implies a reduction per meeting in the monthly purchase pace of $10 billion for Treasury bonds and $5 billion for MBS.

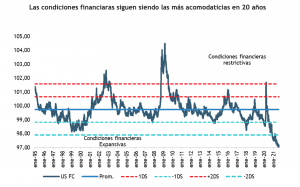

Regardless of how the story ultimately plays out, and barring any major inflationary surprises, the outlook continues to point toward a very gradual normalization that would keep financial conditions fairly accommodative, and despite concerns about the recent downward revision in economic data, we remain confident that strong growth is on the horizon and that economic activity is set to pick up again. We believe the recent slowdown is temporary and is driven primarily by the Delta variant.

We do not expect this wave of COVID-19 to permanently destroy demand, but rather to delay the reopening and economic normalization. In fact, a growing number of indicators point to a turning point for the Delta variant. As long as Covid continues to subside, strong momentum should continue into 2022 as companies begin to rebuild depleted inventories and increase capital spending. Central bank policies should remain growth-oriented, and even the slowdown in China will likely be offset soon by a policy shift.

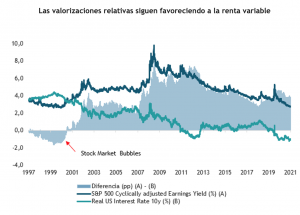

In this context, risky assets would continue to perform well, and bond yields appear to be bottoming out, which generally bodes well for cyclical value stocks.

A final thought. We see a lot of emphasis on high equity valuations, but there is less discussion of how unattractive base rates and corporate spreads are, with little room for them to narrow.

In this regard, we believe the correct approach is to continue overweighting equities relative to fixed income, where relative valuations continue to offer a substantial premium compared to historical levels; meanwhile, for fixed income, we recommend a conservative approach in terms of duration.

Investors should keep in mind that the Fed is moving forward because it has greater confidence in the economy and will continue to provide support. While higher bond yields reduce the relative appeal of stocks, a gradual rise in bond yields should be more than offset by the positive impact of rising corporate earnings as economies return to normal. Therefore, the Fed’s tapering should be viewed as the gradual withdrawal of an emergency support measure as conditions normalize.