Hopes that vaccination will bring an end to the coronavirus pandemic are driving two parallel trends in the U.S. stock market.

First, the prospect of a return to economic normalcy is driving up the stocks of “COVID losers” at the expense of the “COVID winners” that thrived during the pandemic. As a result, oil and gas, retail REITs, airlines, hotels and resorts, and similar sectors are now outperforming tech hardware, online retailers, and gold.

Second, expectations of higher interest rates—as growth prospects are boosted by the vaccine rollout and sustained monetary and fiscal stimulus—are driving up “value” stocks, which are cheap relative to current earnings and can therefore be considered short-term plays. Meanwhile, “growth” stocks—which are expensive relative to current earnings and are therefore long-term plays—are struggling in relative terms. In this environment, the financial sector can provide a hedge against a sharp rise in long-term rates, and the commodities sector can serve as a hedge against rising inflation expectations.

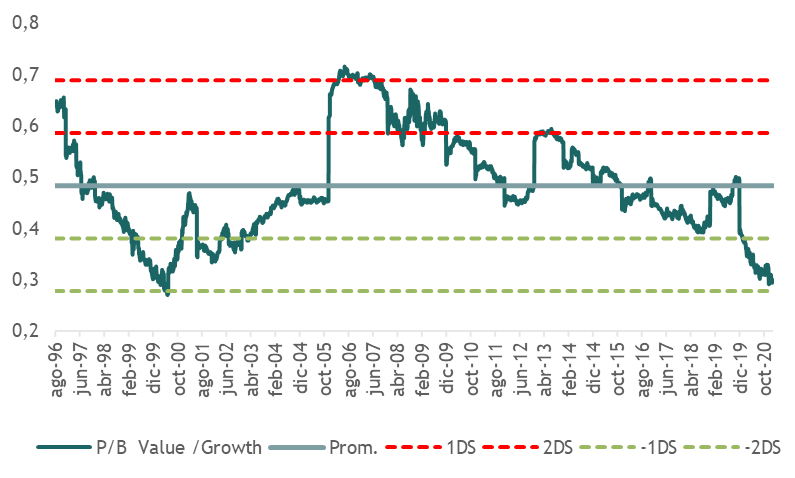

The relative valuations between value and growth stocks remain near 20-year lows.

Relative Valuation: Value vs. Growth

Relative Performance: Value vs. Growth vs. Interest Rates