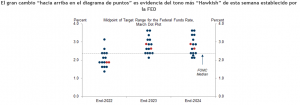

The FOMC raised rates for the first time since the pandemic began and sent a consistently hawkish message at its March meeting. The median projection rose more than expected, pointing to seven rate hikes in 2022 and a terminal rate above the neutral rate of 2.75%.

Nearly half (7 out of 16) of the Committee members expect more than seven rate hikes this year, a fact that was also highlighted by Chair Powell;this lends credence to the idea that at least one 50-basis-point hike is a real possibility later this year.

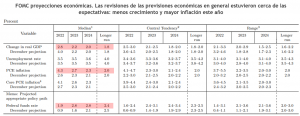

On the economic front, Chairman Powell adopted a more hawkish tone by acknowledging the severity of the inflationary situation during his press conference and emphasizing the strength of the economy—and the labor market in particular— comments that suggest it would take a lot to divert the FOMC from its path of monetary tightening.

Powell said that the FOMC will be “monitoring the risks of further upward pressure on inflation and inflation expectations” and acknowledged that high inflation has spread more widely across the services sector and that wage growth is running at a pace well above what would be consistent with 2% inflation.

Powell also assessed the risk of a recession as “not particularly high,” and emphasized that the average GDP growth forecast for 2022 of 2.8% is 1 percentage point above long-term potential; he highlighted the “tremendous momentum” in hiring and pointed to the gap between job openings and job seekers as evidence that the labor market is “extremely tight.”

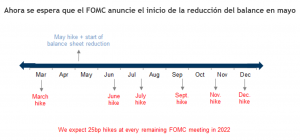

Regarding balance sheet reduction, the FOMC is now expected to announce its start at its next meeting in May, as Powell himself suggested. He also noted that the minutes from this week’s meeting—to be released in three weeks—will reveal some of the key parameters of that process, and that it will be faster than the last cycle but will otherwise seem “very familiar.” This suggests a pace of $60 billion per month for Treasury securities and $40 billion per month for mortgage-backed securities—similar to the last time, but at a faster pace.

Market Outlook and Investment Recommendations

When weighing the negative factors (tighter policies and high valuations) against the positive factors (low risk of recession), investors are advised to maintain a more or less neutral risk exposure. Given current valuations and the prospect of rising yields, investors should maintain a short duration in fixed income, favor value stocks over growth stocks, and overweight banks and the energy and commodities sectors in general.

Humberto Mora

Strategy and Investments