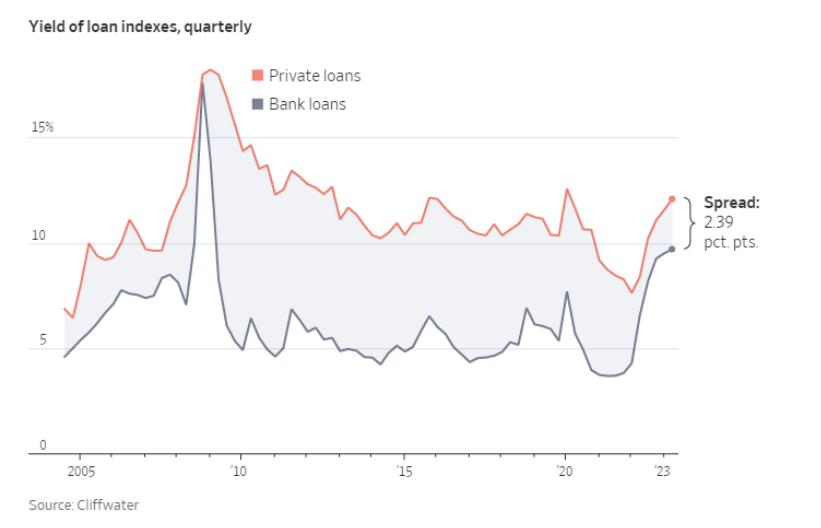

Over the past decade, there has been an upward trend in the private debt industry: while bank loans grew by 180% from 2010 to 2022, this asset class grew by 278%.

This phenomenon began when regulators imposed higher capital requirements on banks in order to ensure the sector’s solvency, as it is essential to the functioning of the economy. Banking regulations have evolved over the years, and following the great financial crisis of 2008, Basel IIIwas implemented—a set of internationally agreed-upon measures designed to mitigate risks inherent in the banking business. These measures, which provide the market with assurance regarding the functioning of the banking sector, ultimately present an opportunity for actors not subject to these regulations.

Looking ahead, the outlook for private debt is positive. The failure of some regional banks in the United States has caused concern among regulators and investors, leading banks to lend less due to a more unstable depositor base, and they are currently building up higher levels of capital reserves in preparation for possible increases in regulatory requirements, given that regulators have already highlighted the importance of holding higher reserves in the wake of the events at the beginning of the year.

On the other hand, there has been lower demand for bank loans because financing has become relatively more expensive than private debt as a result of interest rate hikes in the markets, caused by rising inflation stemming from the COVID-19 pandemic. Furthermore, the outlook for weaker growth is causing banks to adopt a more restrictive stance to avoid losses, thereby limiting their lending.

All of this is reflected in the latest Senior Loan Officer Opinion Survey on Bank Lending Practices (October 2023), which examines changes in standards, terms, and demand for bank loans to businesses and households over the past three months. According to the survey, lending standards for business loans were stricter, and among these restrictions, it is noteworthy that banks may now require higher levels of collateral, a stronger credit history, or more favorable terms before granting loans, coupled with weaker demand for commercial and industrial loans from businesses of all sizes.

However, not everything is risk-free. Private debt faces the same risks as banks, and for the first time, it is also facing an economy with higher interest rates and an economic slowdown that could be prolonged (unlike during the pandemic, when the economy grew rapidly due to fiscal stimulus). As a result, delinquency on these loans is expected to rise, affecting the growth of this asset class. For this very reason, it is important to remain cautious and guard against potential declines in investment value, which is why selecting a good private debt manager is essential when investing.

Vicente Dourthé

Fynsa AGF Private Debt Team