In a changing market, where the outlook for the future is uncertain, securing financing is becoming increasingly difficult, more expensive, and less flexible, which reduces companies' tangible profits.

The word “mezzanine” (from the Italian “mezzanino”) refers to the intermediate level between one floor and another in a building, which vividly describes this type of investment, as it consists of a hybrid strategy that falls between debt and equity. Mezzanine debt is a strategy that yields a return similar to that sought by equity investors, but in terms of payment structure, it takes precedence over shareholders. This is why it is considered a hybrid strategy.

To better understand this, companies have several financing options, with senior debt at one end of the cost spectrum—which refers to traditional bank debt obtained at a lower cost and which has priority in repayment in the event of liquidation. At the other end of the spectrum is equity financing, which is more expensive due to the returns demanded by investors and riskier because it has the lowest priority for repayment in the event of liquidation.

Mezzanine debt falls somewhere between these two options, offering greater flexibility and customization depending on the type of business. “There are three types of mezzanine debt: senior subordinated debt, convertible subordinated debt, and preferred stock; all of these instruments have priority in the event of bankruptcy.” (Eric Novinson, 2014)

In this context, mezzanine debt offers a number of advantages and benefits for companies and their shareholders, as it has more flexible repayment terms that allow it to adapt to business needs—such as deferring interest payments or paying lower interest rates in exchange for a percentage of profits. Furthermore, this alternative is non-dilutive, allowing shareholders to maintain their equity stake. When this type of financing is combined with traditional debt, it reduces the need for capital from shareholders, which improves their return, provides protection, and prevents growth from being hindered during periods of illiquidity.

The most common form of mezzanine financing is subordinated debt, in which the mezzanine lender shares the collateral with the senior debt (e.g., a bank) on a subordinated basis, meaning that the mezzanine lender takes a second-priority claim on the collateral. making it riskier and therefore requiring a higher return; in the event of default, the mezzanine lender has the option to convert the debt into equity to protect its investment.

Other forms of mezzanine financing include convertible loans, in which the lender’s return is tied to the company’s profits. There are also convertible bonds, which, in addition to paying interest and principal, entitle the holder to purchase shares at a specified time.

Global Trends and Local Opportunities

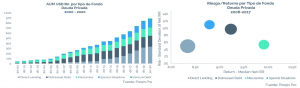

Globally, investment funds focused on mezzanine debt have seen the largest increase in AUM in recent years; according to data provided by Preqin, they rank third in terms of AUM among private debt strategies.

On the other hand, the study conducted by Preqin, based on its database of investment funds worldwide, ranks mezzanine debt as the strategy with the best risk-return profile among private debt funds, where, with an average standard deviation of around 6%, it offers average returns of 9.8%. (See chart) .

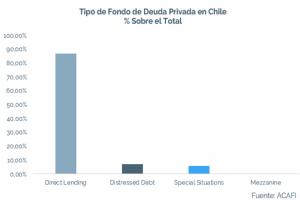

At the local level, this strategy is still in its infancy, with mezzanine debt accounting for less than 2% of the portfolio of public private debt investment funds. In the current climate of uncertainty and rising interest rates, mezzanine debt presents a concrete business opportunity that could meet the needs of both investors and companies seeking financing.