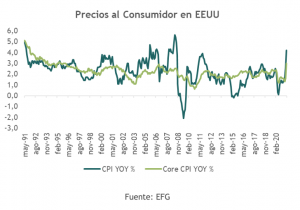

This week’s U.S. CPI release was much stronger than expected. Headline inflation (measured as the year-over-year percentage change in the CPI) reached its highest level since September 2008, and core CPI inflation (excluding food and energy) hit its highest level since 1996. This has reinforced fears of a return to the stagflationary conditions of the 1970s, when high unemployment and high inflation coexisted for several years. Rising commodity prices, supply chain issues (such as those involving semiconductors), declining global trade, and trade rigidities resulting from COVID-19 restrictions are cited as reasons why we should be concerned that the rise in inflation may be more than just temporary.

There are a number of points to keep in mind regarding the published data:

- Inflation was expected to rise sharply in April anyway due to the base effect: year-over-year comparisons are favorable for April and May because the CPI fell sharply during this period last year. This effect will fade in the coming months.

- The impact of the base effect will peak in May, after which it will decline as the year progresses; therefore, if inflation remains high, it will be due to other factors. The May CPI report will be released on June 10, so market jitters over inflation are likely to continue for at least the next couple of months.

- The data is revised frequently. Given the unusual circumstances of last year, the revisions may be quite significant. Yesterday's impact may turn out to be smaller once the final data is released.

- The June CPI report will be released on July 13. Only then will it become clear to what extent higher inflation has been driven by the base effect or other factors. However, uncertainty will remain. Only if inflation falls rapidly and remains low thereafter will fears subside.

- While our fundamental view is that inflation will fall back to levels consistent with the Federal Reserve’s targets, upside risks have increased.

- Central banks have struggled for at least the past decade to boost CPI inflation despite an exceptionally accommodative monetary policy. It is somewhat ironic, then, that now that some inflation has returned, nerves are on edge. While there may be some short-term jitters, inflation that is structurally a bit higher over the next 10 years than it was over the past 10 would not be a bad thing. For example, it would help reduce the real burden of debt—for the government, households, and businesses.

- Several Federal Reserve governors and presidents of regional banks have consistently reiterated a moderate message over the past few months. Even if inflation is slightly above target, that is not a major concern, especially now that there are eight million fewer people employed than at the pre-COVID peak. Furthermore, the Fed has emphasized the importance of how unemployment is distributed across different segments of American society, a factor that also allows for a high degree of flexibility.

The risks of persistently higher inflation have certainly increased recently, and it is natural to worry that the temporary factors driving up inflation will not subside as much as pure statistical models suggest. However, we expect inflation to ease to more comfortable levels in the second half of the year. This will not become apparent until mid-July. Until then, markets are likely to be sensitive to news flows that are perceived as supporting the high-inflation hypothesis. If we are wrong and inflation remains persistently higher, we expect the Federal Reserve to be patient in winding down stimulus.