A CLO, or Collateralized Loan Obligation, is a type of financial instrument used to finance corporate loans.

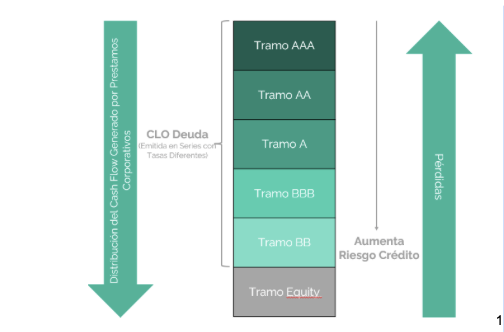

CLOs are issued through a specialized vehicle that pools loans and divides them into different tranches based on their risk level. Investors who purchase CLO tranches receive cash flows from the underlying loans and, in some cases, a share of the appreciation in the value of the loans.

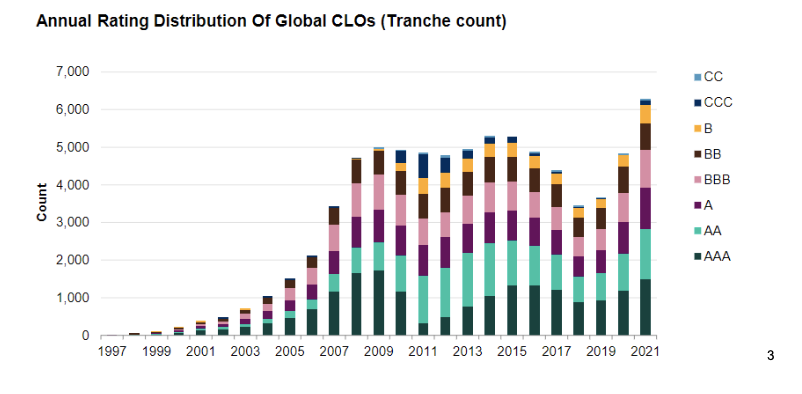

The first CLO was issued in the 1980s, and since then the market has grown significantly, especially in the United States. One of the main characteristics of CLOs is that they are used to purchase and finance corporate loans with varying levels of risk, while also highlighting their scope and diversification—which generally cannot be achieved by an individual investor.

CLOs are also structured so that the cash flows from the underlying loans are divided into different tranches, allowing investors to choose their desired level of risk and return.

Although CLOs can offer attractive returns, they also carry significant risks. One of the biggest risks is the risk of default, since the underlying loans are often made to companies that are at a higher risk of being unable to repay them.

In addition, CLOs are also exposed to macroeconomic risks, such as economic recessions and changes in interest rates. It is important to note that changes in interest rates can also affect the valuation of CLOs.

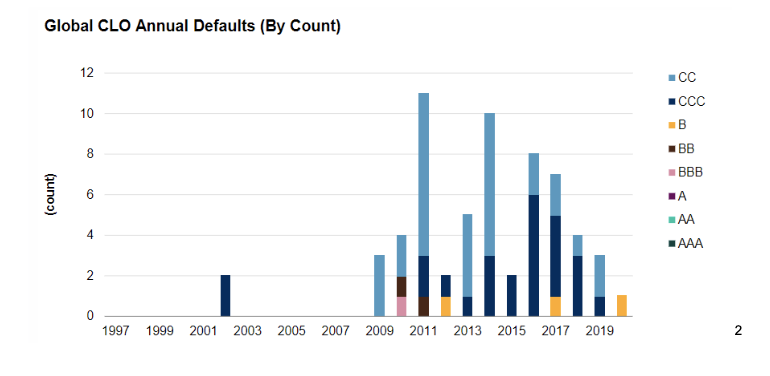

On the other hand, between 2019 and 2020, there were only 4 CLO defaults, and about 10% saw their credit ratings downgraded. Notwithstanding the above, the historical average default rate is less than 1%.

Moody’s estimates that a potential recession in the U.S. in the second quarter of 2023, coupled with GDP growth of 0.4%, would result in a default rate among the lowest-rated issuers of around 5% (compared to the previous 12 months, which saw a default rate of 1.0%).

These defaults coincide with rating downgrades for issuers, particularly in the BBB through CCC tranches.

The CLO market is regulated by the Securities and Exchange Commission (SEC) in the United States. In addition, many institutional investors, such as pension funds and hedge funds, have specific requirements for investing in CLOs. The leading CLO managers and issuers include Blackstone, the Carlyle Group, and KKR, among others.

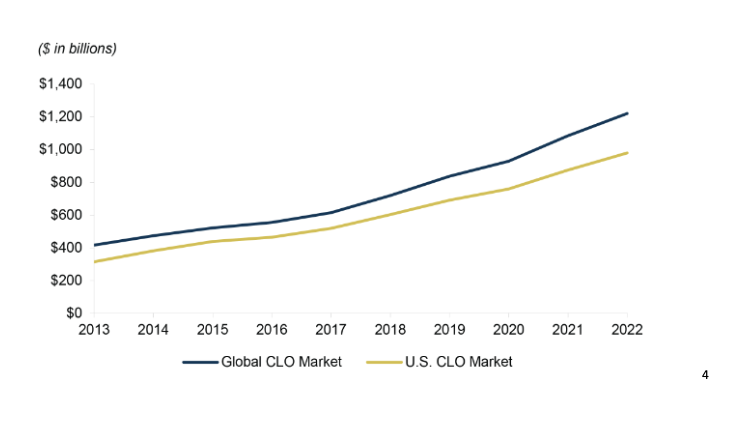

The CLO market in the United States is large and complex. In 2020, more than US$125 billion in CLOs were issued in the United States. However, the market has also been the subject of criticism and a lack of regulation due to its role in the 2008 financial crisis.

Despite these risks and challenges, CLOs remain an important source of financing for high-risk companies and an investment option for institutional investors.

Martín León

Assistant Manager of International Funds, Fynsa AGF