As we have mentioned in previous reports, historically, peak inflation has triggered a pullback in risk assets and the bond market, provided that a recession does not occur. On average, stocks have declined as inflation rises and approaches its peak, but they can rebound beyond previous highs—especially if a recession is avoided—and stocks clearly outperform bonds in this scenario. In other words, if growth remains strong enough, a shift in inflation momentum may signal a market bottom. However, the risk of equity declines remains high if a recession materializes, and equities may remain under pressure for another 6 months or so after inflation peaks: on average, the trough in economic activity data occurs between 6 and 8 months after inflation has peaked.

The trend for U.S. 2-year rates was clearly downward, with the federal funds rate falling in 7 of the 11 instances of peak inflation since World War II. With inflation reaching much higher levels, the risk of persistent inflation is greater today, which could mean continued tightening by the Fed despite falling inflation and the persistent risk of recession (further reaffirmed in the minutes released this week).

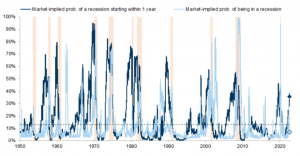

In fact, the market-implied probability of a U.S. recession in the next 12 months has remained high (see Chart No. 1), while the probability implied by risk assets of being in a recession has fallen sharply (see Chart No. 2), as markets have rebounded. In other words, markets have priced out the risk of an imminent recession, but latent risks remain high.

Source: Fynsa Estrategia; Bloomberg

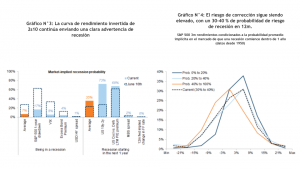

Source: Fynsa Estrategia; BloombergMeanwhile, the U.S. yield curve remains deeply inverted and still points to persistent risks of a recession (see Chart No. 3). Furthermore, the signal from the 12-month implied change in the federal funds rate is distorted, as markets are pricing in large rate hikes through the end of this year, before cuts begin next year; historically, the way markets price in Fed rate cuts is more consistent with the elevated risk of recession triggered by a more restrictive central bank.

And bear markets in stocks generally end with a steepening yield curve that coincides with a final drop in stock prices; without that signal, the risk of a decline remains high. As noted in a recent Goldman Sachs report, if the probability of a recession in the next 12 months is above 40%, the risk of market corrections is higher than normal: current levels stand at 37% (see Chart No. 4).

A final thought on the concept currently in vogue in the markets: the “Fed pivot.” In this regard, the experience of 2019 is interesting, as markets fell sharply in Q4 2018 because the Fed intended to continue raising interest rates in 2019 to restrictive territory (from “neutral” territory, as they were then, just as they are now), in addition to beginning to reduce its balance sheet. Well, that never happened; the market decline ultimately tipped the scales toward easing, long-term inflation expectations fell as low as 1.6%, and the Fed managed to avert a recession with an “effective pivot” in policy (cutting rates by 75 basis points in 2019). Then came the COVID-19 recession, but that’s another story.

The reality today is quite different. While inflation expectations implied by the bond market have moderated, actual inflation remains high, and unlike in 2019—when the market recovery coincided with a sharp shift in 2-year rates (clearly signaling that the Fed would cut interest rates)— what we see today is that risk assets have recovered substantially, while interest rates—though they have not reached new highs—do not show a greater tendency to fall either, which keeps the yield curve inverted. (See Chart No. 5).

However, unless the “peak inflation” narrative is confirmed by both the data and a moderate policy pivot by the Fed, we believe that the risk of a return of rate shocks and fears of a recession may once again weigh on risk appetite.