July business surveys provide a clearer picture of a global slowdown. The global all-industry PMI fell sharply (including China), more than reversing June’s gain and falling to its lowest level of the expansion. At 50.8, J.P. Morgan’s manufacturing PMI—the single best indicator of global activity—fell 2.7 points from June to a level consistent with annualized global GDP growth of 2.2%. While the implied rate of global GDP growth from the PMIs (2.2%) is slightly below potential (2.6%), the surveys do not yet signal the kind of sharp downturn that would be expected if the global economy had entered a recession, as many fear.

That said, this does not mean there are no causes for concern, as the surveys highlight a number of weak spots. Along with a further decline in orders and future growth expectations to expansionary lows, there are worrying signs that labor markets may be struggling more than expected. Combined with a widespread decline across all sectors and countries, the July surveys underscore the increased risk of a recession by midyear.

By sector, both manufacturing and services appear to have slowed. The global manufacturing PMI fell 2.4 points last month to a level consistent with stagnant growth in the industrial sector. At the same time, the decline in the manufacturing PMI for new orders and the increase in the inventory PMI suggest that global manufacturing has already contracted.

Meanwhile, the services PMI fell sharply last month by 2.8 points. While the decline is partly due to a surprisingly large drop of 5.4 points in the U.S. services PMI (which contrasts sharply with the increase reported in the non-manufacturing ISM, which, unlike the PMI, also includes government, construction, and mining), significant declines were reported in all reporting countries except China and Russia.

A welcome development in the latest surveys is the signs that inflationary pressures are easing. Price indices remain high, but the declines are encouraging. However, even these signs come with a caveat: the decline in the PMI for input and output prices across the entire industry could be as much (or more) a sign of weakening demand as it is of improving supply.

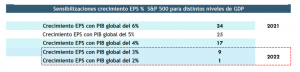

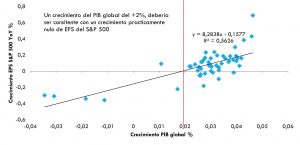

Finally, the sharp slowdown in global growth serves as a reminder that the market may be overly optimistic about expected earnings growth for 2022 and 2023. Global growth closer to 2% should be consistent with zero earnings growth for the S&P 500, while the market continues to expect growth closer to 10%.